During the first half of 2025, the U.S. construction market lost some momentum. Economic uncertainty, elevated costs and shifting tariff policies prompted some projects to be delayed until conditions become clearer. While contractors remain cautiously optimistic about the second half of 2025 due to certain policy changes from the Trump administration, forecasters anticipate economic headwinds to persist and weigh on construction starts, which are projected to decline over the course of the year, with the slowdown most pronounced in nonresidential segments sensitive to financing and policy risk. However, the U.S. data center and mission-critical facilities market continues to expand, driven by surging demand from AI adoption, cloud computing expansion and hyperscale demand.

Recent Industry Performance

During 2024, total U.S. construction starts rose 6.0% from 2023 to reach $1.15 trillion, according to Dodge Construction Network (“Dodge”). Specifically, residential starts grew 7.0% and nonresidential starts increased by 4.0%, while nonbuilding starts expanded by 7.0%. Then, during the first six months of 2025 (latest available), total U.S. construction starts reached a value of $576.0 billion, up 0.9% from the same period in 2024. Nonresidential starts gained 6.2% and nonbuilding starts increased 1.5% year-over-year, while residential starts fell 5.1%.

“Construction starts saw solid growth in June, alongside particular strength in manufacturing and data center construction,” says Sarah Martin, associate director of forecasting at Dodge. “However, risks remain elevated that construction starts will be more subdued in the back half of the year—alongside ongoing uncertainty over trade policy and the broader economy.”

Project information firm ConstructConnect concurs with this sentiment, noting that “the worsening economic outlook, tariff uncertainty, and rising inflationary costs” caused them to downgrade their forecast for the U.S. construction industry this year. Indeed, in their Summer 2025 “Construction Starts Forecast,” the firm notes, “Many businesses are delaying planned investments as they wait for this period of uncertainty to pass.” Overall, total U.S. construction starts are forecast to decline by 1.8% in 2025. While heavy/civil engineering construction will likely remain the strongest segment, it is expected to stagnate during the year. Meanwhile, ConstructConnect anticipates that both residential and nonresidential construction starts will fall.

Nonresidential Construction

As mentioned previously, Dodge reports that, during 2024, U.S. nonresidential construction starts grew by 4.0% when compared to 2023, reaching $434.1 billion. Within this segment, commercial starts rose 8.0%, institutional starts increased 16.0% and manufacturing starts declined 35.0%. Then, during the first half of 2025 (latest available), nonresidential starts totaled $220.0 billion, up 6.2% from the first half of 2024. Commercial and industrial starts grew 9.0% during the six-month period, while institutional starts rose 3.0%.

Meanwhile, ConstructConnect has a different perspective on nonresidential building starts in 2024. The firm indicates that nonresidential building starts totaled $377.4 billion in 2024, down 8.5% from 2023. Broken down further, ConstructConnect estimates that commercial starts saw a 4.8% increase, institutional starts rose by 7.2% and manufacturing starts fell by 51.3%. For the first half of 2025 (latest available), ConstructConnect reports that nonresidential building starts totaled $215.0 billion, up 11.5% from the first half of 2024, with commercial starts up 4.3%, institutional starts down 4.1% and manufacturing starts up 77.2%.

Moving forward, ConstructConnect projects that nonresidential building starts will decrease by 3.9% in 2025, which would be a slight improvement from the activity seen in 2024. However, the firm notes that these declines were experienced following very strong post-pandemic construction activity. They point to the manufacturing sector as a prime example; indeed, manufacturing starts expanded 229.0% in 2022, which made the declines of 2023 and 2024 “highly expected.” Overall, ConstructConnect anticipates that commercial construction will grow by 7.4% in 2025, with robust growth for transportation terminals and private offices. Meanwhile, manufacturing starts are forecast to decline by 9.3%, and institutional starts will likely fall by 11.8%. Notably, the projected decline for institutional starts would be the first year of contraction since 2022. While the nursing homes, police/fire, and military subsectors are anticipated to see growth, this is expected to be offset by declines in the construction of prisons, hospitals and clinics, and educational facilities.

Looking further ahead, ConstructConnect forecasts that nonresidential building construction starts will decline by 3.0% in 2026. However, in 2027, 2028 and 2029, starts are projected to expand by 4.5%, 4.7% and 4.2%, respectively.

Residential Construction

Residential construction starts expanded by 7.0% in 2024, reaching $389.2 billion. Dodge indicates that single-family starts were up 15.0%, while multifamily starts declined by 7.0%. Then, during the first six months of 2025 (latest available), residential starts totaled $192.0 billion, down 5.1% from the same period in 2024, with single-family starts declining 11.0% and multifamily starts increasing 8.0%.

Meanwhile, the National Association of Home Builders (“NAHB”) reports that, during 2024, total housing starts reached 1.36 million, down 3.9% from 2023 when housing starts totaled 1.42 million. Broken down further, single-family starts were up 6.5% from 2023, while multifamily housing starts were down 25.0%. Then, during the first six months of 2025 (latest available), housing starts saw the following pattern: down 9.8% in January; up 11.2% in February; down 11.4% in March; up 1.6% in April; down 9.8% in May; and up 4.6% in June. During June 2025, housing starts reached a seasonally adjusted rate of 1.32 million units, with single-family starts down 4.6% to a seasonally adjusted annual rate of 883,000 and multifamily starts up 30.0% to an annualized pace of 438,000. Notably, during June 2025, single-family starts were down 10.0% from June 2024.

In July 2025, Robert Dietz, chief economist for the NAHB, reported that due to high interest rates and the effect of policy uncertainty on potential home buyers, the NAHB lowered their expectations for single-family home construction. Dietz says, “Right now, we are expecting single-family housing starts to be down about 5% in 2025. That’s a contrast from the beginning of the year, when we expected starts to be flat.”

Meanwhile, ConstructConnect projects that 2025 will be the third consecutive year of declines for residential construction starts, with the segment anticipated to fall by 0.8%. While single-family starts will likely achieve 0.6% growth during the year, primarily due to rebuilding efforts following a year of natural disasters throughout the U.S., multifamily starts are anticipated to drop 3.9% as a result of high financing costs. However, looking further ahead, ConstructConnect forecasts that residential construction starts will grow by 6.1% in 2026, 7.4% in 2027, 6.1% in 2028 and 7.3% in 2029.

With regard to the remodeling market, according to the Leading Indicator of Remodeling Activity, published by the Remodeling Futures Program (“RFP”) at the Joint Center for Housing Studies of Harvard University, spending on home improvements and repairs is forecast to soften in 2026, increasing by an anticipated 1.2% by the second quarter of the year. “Weakness in the current housing market is expected to have a dampening effect on home improvement spending,” notes Rachel Bogardus Drew, director of the RFP. “Slowing construction starts and remodeling permitting activity, which are key factors in predicting future remodeling expenditures, are also putting downward pressure on home improvement growth.”

Nonbuilding Construction

Nonbuilding construction starts grew by 7.0% in 2024 to reach a total of $324.3 billion, according to Dodge. Specifically, highway and bridge starts rose 6.0%; environmental public works starts gained 24.0% and miscellaneous nonbuilding starts increased 26.0%. Meanwhile, utility/gas plant starts fell 14.0%. Then, during the first half of 2025 (latest available), nonbuilding construction starts totaled $164.0 billion, up 1.5% from the same period in 2024, with miscellaneous nonbuilding starts up 17.0%, highway and bridge starts up 8.0%, utilities starts down 15.0% and environmental public works starts down 1.0%.

At the same time, ConstructConnect reports that heavy/civil engineering starts totaled $273.9 billion in 2024, up 12.1% from 2023. Then, during the first six months of 2025 (latest available), heavy/civil engineering starts reached a value of $158.1 billion, up 6.5% from the first half of 2024. Specific segments performed as follows in the first six months of the year when compared to the same period in 2024: airport, up 54.1%; road/highway, up 2.0%; bridge, up 29.5%; dam/marine, up 37.5%; water/sewage, up 2.8%; electric power infrastructure, down 43.6%; and all other civil, up 23.9%.

In recent years, funding for infrastructure projects expanded under the Infrastructure Investment and Jobs Act of 2021 and the Inflation Reduction Act of 2022. However, in 2025, President Trump took several actions that paused distributions of funding or halted executions of programs, many of which involved clean energy. In some cases, these moves were judicially blocked. Nonetheless, the nonbuilding construction sector experienced project delays in some cases.

At the same time, the Trump administration is prioritizing infrastructure construction in some of its moves. Transportation Secretary Sean Duffy remarked at an infrastructure conference, “We want to streamline the rules and regulations around what you do as much as possible.” Duffy’s “America Is Building Again” agenda includes accelerating project delivery for transportation projects, enhancing safety, strengthening partnerships with states, reforming the National Environmental Policy Act and increasing the use of technology.

Moving forward, ConstructConnect projects that heavy/civil engineering starts will stagnate in 2025. However, the firm notes, “This is largely a normalization of the strong growth in the sector in recent years.” During the year, road construction starts are expected to rise by 8.3%, while bridge construction starts will likely grow by 12.7%. Other subsectors are forecast to decline: miscellaneous civil, which includes power, oil and gas as well as tunnel projects (-12.6%); marine (-21.5%); airport (-1.9%); and water and sewage treatment (-4.0%). Looking further ahead, ConstructConnect anticipates that heavy/civil engineering starts will return to growth in 2026, expanding at an estimated rate of 4.7%. Thereafter, starts are expected to experience 4.5% growth in 2027, 3.4% growth in 2028 and 3.2% growth in 2029.

Construction Industry Trends/Drivers

Construction Input Prices

The U.S. Bureau of Labor Statistics (“BLS”) reports that, after construction input prices declined slightly in December 2024, prices surged during the first quarter of 2025. Indeed, construction input prices expanded at a 9.7% annualized rate through the first three months of the year. While materials prices decreased by 0.1% month-over-month in April 2025, prices rose by 0.2% in both May and June 2025 (latest available). Notably, nonresidential construction input prices accelerated at a 6.0% annualized rate during the first six months of 2025. Nonetheless, prices for several of the inputs that are directly impacted by tariffs, such as iron and steel, decreased in June 2025. Overall, the BLS indicates that construction input prices were 2.1% higher in June 2025 than they were in June 2024 and remained 42.1% above prices in February 2020, prior to the start of the COVID-19 pandemic. According to Anirban Basu, chief economist at Associated Builders and Contractors (“ABC”), “While it is unclear how and when trade policy will affect construction materials prices, the impact was evident in June’s Consumer Price Index release; prices for core goods excluding automobiles rose at the fastest pace since late 2021.” Basu continues, “Economic uncertainty remains extraordinarily elevated.”

Labor Issues

Construction employment increased by 2,000 jobs on net in July 2025 (latest available), according to the BLS. On a year-over-year basis, industry employment grew by 96,000 jobs, or 1.2%, mainly due to expansion on the nonresidential and nonbuilding sides of the industry. At the same time, the unemployment rate for the construction industry was unchanged at 3.4%. “The construction industry has added just 7,000 jobs over the past four months,” notes ABC’s Basu. “Industrywide employment is up only 1.2% over the past year, a lackluster pace of growth that historically is seen during and immediately following recessions. The good news for ABC members is that the nonresidential segment continues to outperform, growing at twice the pace of the industry at large over the past 12 months. Given that ABC member backlog remains healthy and hiring expectations remain relatively optimistic, according to ABC’s Construction Backlog Indicator, it’s possible that weakness will be confined to the residential side of the industry during the second half of 2025.”

Construction Backlog

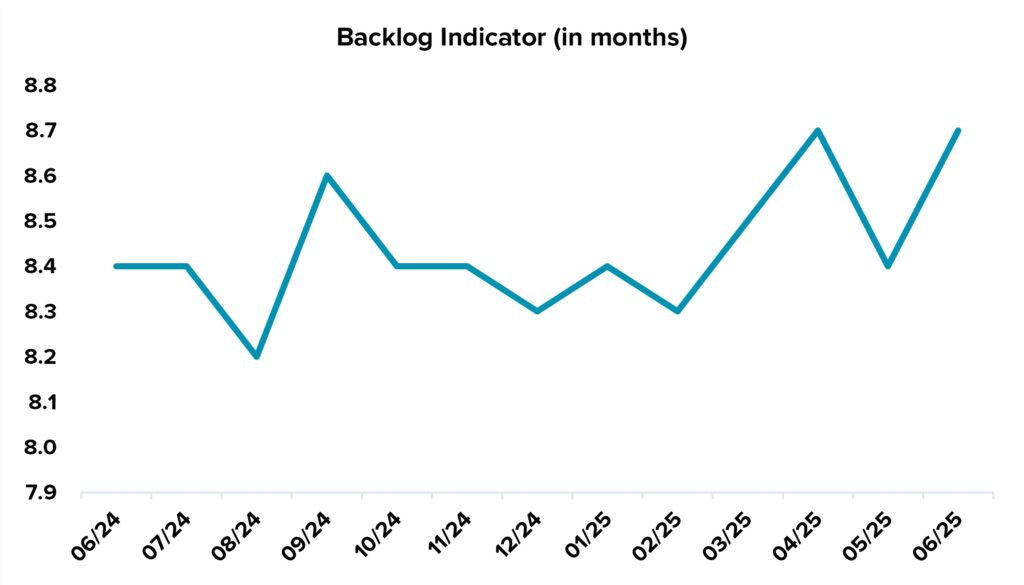

ABC reports that their “Construction Backlog Indicator,” which includes commercial, institutional, heavy industrial, and infrastructure construction, was at 8.7 months in June 2025 (latest available), up from 8.4 months in May 2025 and 8.4 months in June 2024. Specifically, by industry, commercial and institutional construction had a backlog of 8.9 months in June 2025, up slightly from 8.8 months in May 2025 and up from 8.5 months in June 2024. Heavy industrial construction registered a backlog of 6.8 months in June 2025, down from 7.2 months in May 2025 and 9.6 months one year prior. Meanwhile, during June 2025, infrastructure construction had a backlog of 9.3 months, up from 6.8 months in May 2025 and 8.2 months in June 2024. Moreover, ABC reports that backlog improved between June 2024 and June 2025 for contractors with annual revenue under $30.0 million and over $100.0 million, whereas for those with revenue between $30.0 million and $100.0 million, backlog fell. Overall, ABC’s Basu notes, “Despite a wide array of headwinds and disappointing construction spending data in recent months, backlog rebounded to 8.7 months in June, the same level as in April. The durability of contractor backlog is partially due to the ongoing boom in data center construction; 1 in 7 ABC members is currently under contract to perform work on a data center.”

Construction Confidence Index

All three metrics measured by ABC’s “Construction Confidence Index”—sales, profit margins and staffing—remained above 50.0 in June 2025 (latest available), which indicates that contractors anticipate growth during the second half of the year. The sales index was up compared to both May 2025 and June 2024, while the index for profit margins expanded slightly compared to May 2025 but was down slightly compared to one year prior. Meanwhile, during June 2025, the staffing index was down both month-over-month and year-over-year. ABC’s Basu says, “[Contractors] remain broadly optimistic, with 3 in 5 contractors expecting their sales to rise during the second half of 2025.” However, Basu indicates that the survey was taken prior to certain trade policy announcements. Notably, one in five contractors experienced project interruptions or had a project paused in June 2025 due to tariffs. According to Basu, “With some of the newest import taxes putting upward pressure on construction input prices, profit margin expectations may face pressure in the months to come.”

One Big Beautiful Bill Act

The One Big Beautiful Bill Act, passed in July 2025, is expected to significantly boost construction activity across the U.S., according to Construction Dive. Key provisions include the restoration of 100.0% bonus depreciation, a permanent extension of the 20.0% pass-through deduction under Section 199A and the immediate expensing of research and development costs. These changes are beneficial for construction activity, particularly for small and mid-sized contractors, due to the fact that they are expected to improve cash flow and enable investments in safer, more efficient equipment. John Robbins of real estate and infrastructure consultancy firm Turner & Townsend notes that “these tax enhancements should be very attractive and help greenlight shovels in the ground throughout the country.” Sectors likely to benefit most include manufacturing, defense infrastructure, border security—supported by nearly $50.0 billion in funding—and domestic energy production. However, the anticipated surge in activity may exacerbate existing pressures on the construction labor force and supply chains, especially given the bill’s emphasis on domestic sourcing. With tax credits for energy-efficient buildings expiring after 2026, firms are expected to accelerate project timelines to maximize benefits.

NAHB Builder Confidence Survey

According to the most recent NAHB/Wells Fargo Housing Market Index (“HMI”), builder confidence received a slight boost in July 2025 due to the passage of the One Big Beautiful Bill Act. However, headwinds, such as elevated interest rates and economic and policy uncertainty, caused the HMI to remain well below the 50.0 mark. Indeed, the HMI rose one point to 33.0 in July 2025. (The HMI measures builder perceptions for the following six months on a scale of “good,” “fair” or “poor.” Any reading below 50.0 indicates that builders view the outlook as negative.) Further, two of the three indices of the HMI registered growth in July 2025; the index for current sales conditions was up one point to 36.0, while the index for sales expectations in the next six months was up three points to 43.0. However, the index charting traffic of prospective buyers declined by one point to 20.0, the lowest reading since the end of 2022. “The passage of the One Big Beautiful Bill Act provided a number of important wins for households, home builders, and small businesses,” notes Buddy Hughes, chairman of the NAHB. “While this new law should provide economic momentum after a disappointing spring, the housing sector has weakened in 2025 due to poor affordability conditions, particularly from elevated interest rates.”

Federal Reserve Rates

The Federal Reserve’s decision in late July 2025 to keep its benchmark interest rate unchanged at 4.25% to 4.50% has extended uncertainty for the construction industry, where high borrowing costs continue to strain project feasibility, according to Construction Dive. Builders had hoped a rate cut would jumpstart stalled projects, but firms are adapting with new strategies. Contractors like Adolfson & Peterson have leaned on public-private project blends, while others, such as GCM Contracting Solutions (“GCM”), are focusing on design-build models and self-performing work to maintain control over speed, costs and scheduling. “Clients [are] looking to preserve flexibility, whether that means phasing a project, streamlining specifications or delaying vertical construction,” says Robert Brown, CEO of GCM. Inflation also remains a key concern. Some contractors are shifting toward public-sector work backed by federal and local funding, which offers more predictable financing amid tightening credit. Despite the uncertainty, others like national builder, developer and real estate manager Ryan Companies continue progressing where conditions align, with President of Southeast Region Patrick Chesser noting, “We do not expect a significant shift in our project pipeline” if rates remain steady.

Recent M&A Trends for the Construction Industry

According to Dealogic,global mergers and acquisitions (“M&A”) totaled $2.14 trillion from January 1, 2025, through June 27, 2025 (latest available), up 26.0% year-over-year. However, fewer deals occurred. Indeed, during that period, there were 17,528 deals signed compared to the 20,583 deals signed during the same period in 2024. Despite the decline in M&A volume, the number of $10.0 billion-plus deals rose 62.0%, which pushed the total value of deals higher than it had been during the first half of 2024. North America recorded US$1.04 trillion in activity, a 17.0% increase, while Asia more than doubled to US$583.9 billion, led by Japan and China. Bankers cited improved market conditions, reduced volatility and looser U.S. antitrust policies as factors increasing the likelihood of megadeals exceeding US$50.0 billion.

Meanwhile, PwC reports that the construction and engineering sector saw moderate M&A activity in the first half of 2025, driven by demand in infrastructure investment despite economic pressures. Buyers targeted scalable platforms, labor efficiencies and resilient end markets, with consolidation notable in trades such as HVAC, plumbing and roofing. S&P Global Market Intelligence data shows deal value at approximately $20.0 billion in the first quarter, with second-quarter-to-date levels trending lower.

At the same time, the Boston Business Journal reports that private equity’s (“PE”) growing footprint in the construction industry is being fueled by demographic, economic and operational factors. An aging workforce and widespread succession challenges have created opportunities for well-capitalized investors to acquire companies lacking viable internal transition options. Additionally, Construction Briefing notes that with over $2.0 trillion in “dry powder” available, PE firms are targeting specialized, high-demand segments—such as mechanical, electrical, plumbing, HVAC and solar contractors—where constrained labor and federal infrastructure spending promise strong backlogs. Once a platform company is acquired, PE buyers often pursue roll-up strategies, consolidating smaller firms to gain economies of scale, expand services and improve pricing power. These dynamics, coupled with strategic plays from industry incumbents, point to continued robust deal activity and consolidation in 2025.

The following are several notable transactions that took place in the construction and engineering industry in the first half of 2025:

- Flatiron and Dragados North America Integration – On January 17, 2025, FlatironDragados unveiled the successful integration of the two companies, which was initially announced in July 2024. This integration makes FlatironDragados the second-largest civil engineering and construction company in North America. The newly integrated company is majority owned by DRAGADOS, S.A., a Spanish construction firm and subsidiary of ACS Group, and HOCHTIEF, a German-based global construction company. According to Juan Santamaria, CEO of ACS Group and HOCHTIEF notes, “With the successful integration of FlatironDragados, we are set to redefine engineering and construction in North America, unifying the complementary strengths of two industry leaders to deliver outstanding outcomes for our clients, people and communities. Through strengthened collaboration and an expanded geographic footprint, we are more equipped than ever to deliver complex, large-scale projects across the United States and Canada.”

- Graham Group (“Graham”) Acquires XL Industries (“XLI”) – On March 4, 2025, Graham, an employee-owned North American construction solutions partner, announced its acquisition of northern California-based construction company XLI for an undisclosed amount. According to Andy Trewick, CEO of Graham, “This merger is an exciting step forward for both companies…By joining forces, we’re growing our market presence and bringing even more innovation to the industry. XL Industries is known for its reliability and commitment to quality, just like us, making this partnership a great fit for both teams. There is no question that our combined strength, talent, and innovation will grow our leadership in the industry.”

- Eaton Acquires Fibrebond – On April 1, 2025, Eaton, an intelligent power management company, acquired Fibrebond, a designer and builder of pre-integrated modular power enclosures, for $1.4 billion. “Acquiring Fibrebond’s innovative and customer-focused business is a game-changing move that positions Eaton as a one-stop shop to rapidly deploy power infrastructure where it’s needed,” says Mike Yelton, president of Eaton’s Americas Region, Electrical Sector. “Their engineered-to-order power enclosures and service capabilities enhance our offerings, allowing us to move faster for our data center, industrial, utility and other customers. We couldn’t be more excited to add this critical capability for our customers in these growth markets.”

- QXO, Inc. (“QXO”) Acquires Beacon Roofing Supply, Inc. (“Beacon”) – On April 29, 2025, building products distributor QXO announced it completed its acquisition of Beacon for approximately $11.0 billion, which makes QXO the largest publicly traded distributor of building products (roofing, waterproofing and complementary building products). According to the Chairman and CEO of CXO Brad Jacobs, “Acquiring Beacon is a major step forward in our strategy to make QXO the leading tech-enabled company in the $800 billion building products distribution industry. We’re excited to welcome Beacon’s talented team and, together, apply our proven playbook to accelerate growth, expand margins, and create an unmatched customer experience.”

Looking ahead, Reuters reports optimism from top bankers for M&A activity in the second half of 2025. Despite a first half riddled with macroeconomic pressures, more than a dozen top bankers shared growing confidence that “the worst of the market turbulence is over.” Indeed, Ivan Farman, co-head of global M&A at Bank of America, states, “There were a lot of deals that were put on hold that will come back…I’m optimistic about the second half [of 2025].”

However, PwC has a more cautious outlook for the construction and engineering market for the remainder of 2025, with “buyers continuing to target scalable platforms tied to residential and institutional demand. Labor constraints and cost pressures persist across the board. Early signs of tariff stabilization may offer greater certainty for buyers and sellers alike.”

Data & Resources

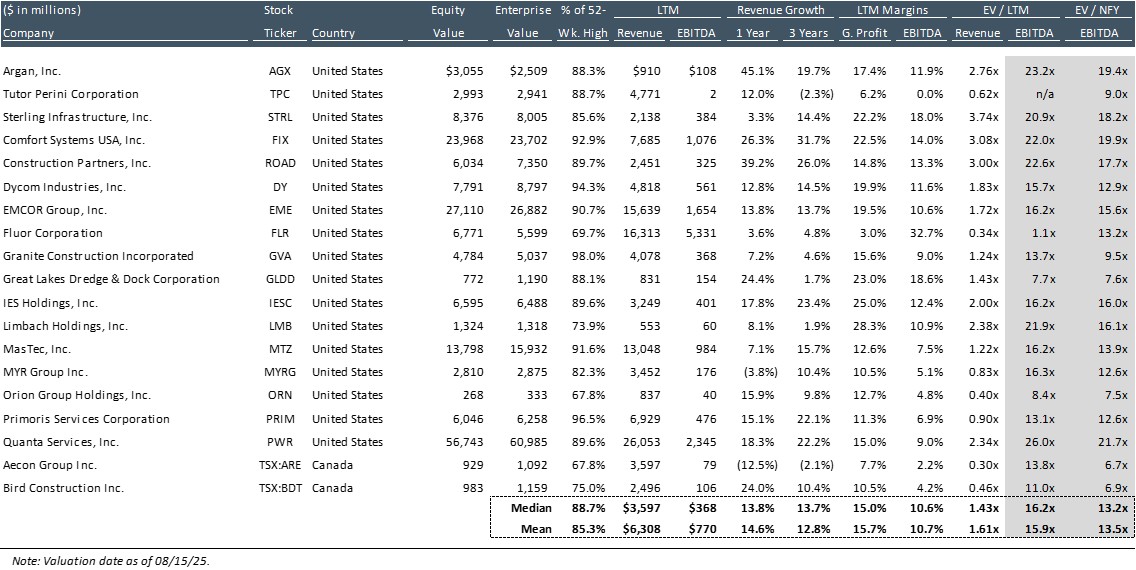

Publicly-Traded Construction Companies

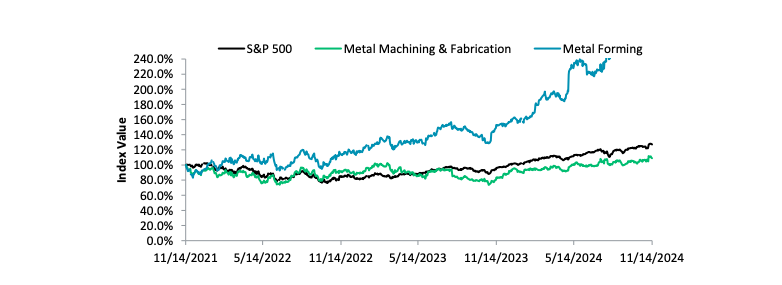

Construction Index Performance vs. S&P 500

Sources: S&P Capital IQ and public data

The Construction Comps Index has significantly outpaced the S&P 500 since 2020, supported by record infrastructure spending, robust housing and industrial demand, and rapid investment in clean energy projects. More recently, the surge in AI-driven data center development has emerged as a powerful driver, reinforcing the sector’s strong growth trajectory and positioning construction firms ahead of the broader market.

Construction Industry Trends

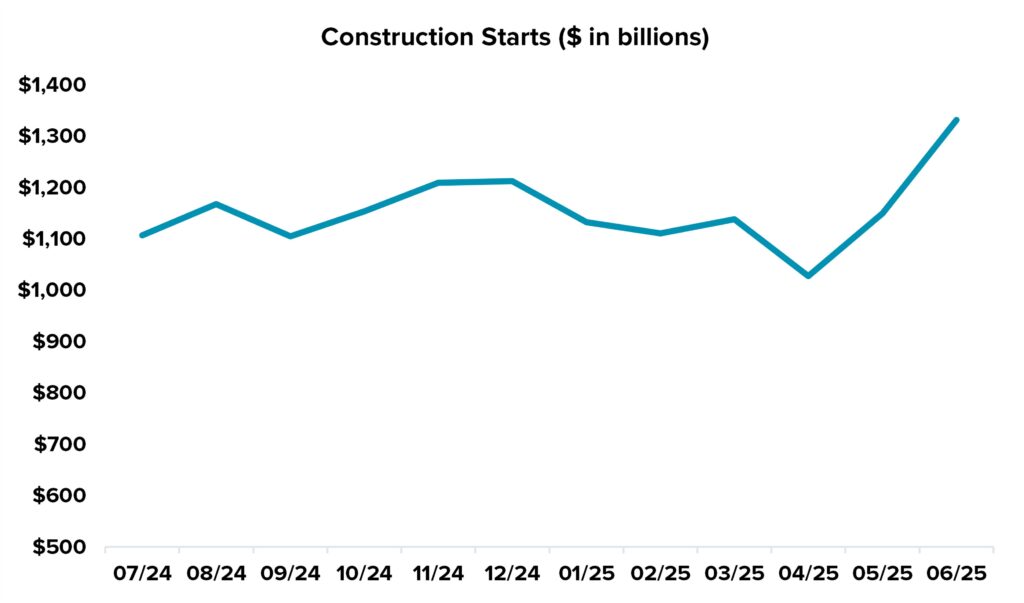

Construction Starts

Source: Dodge Data & Analytics

Dodge Data & Analytics measures the seasonally-adjusted value of total U.S. construction starts each month, as well as the value of starts in nonresiden-tial, residential and nonbuilding categories.

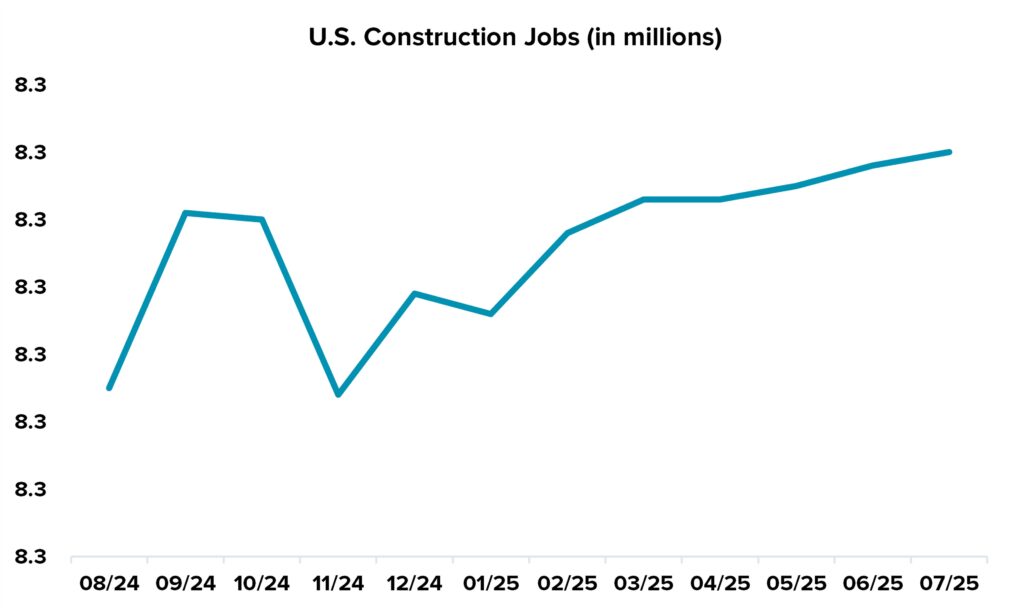

U.S. Construction Jobs

Source: Bureau of Labor Statistics

The Bureau of Labor Statistics releases job gains or losses in the industry and divides the figures into residential and nonresidential sectors.

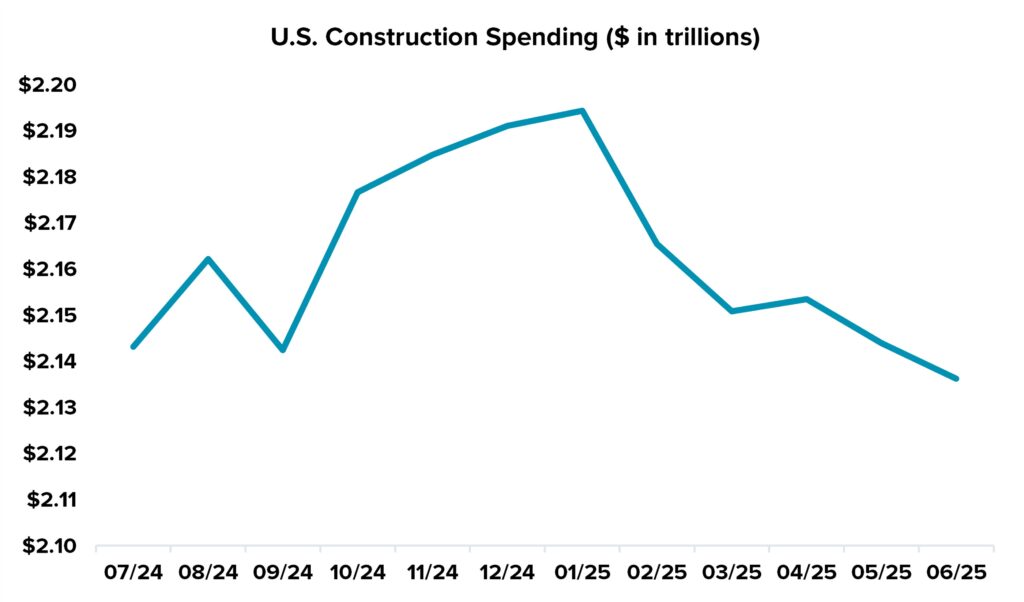

U.S. Construction Spending

Source: U.S. Census Bureau

While often revised in subsequent months, construction spending figures each month from the U.S. Commerce Department examine the private and public construction sectors. Within the private sector, the report tracks single-family residential, multifamily residential and nonresidential starts.

Backlog Indicator

Source: Associated Builders and Contractors

The Associated Builders and Contractors’ backlog indicator is a forwardlooking economic metric that reflects the amount of work under contract that will be performed by commercial and industrial construction contractors in the months ahead.

Notable Closed M&A Transactions — Construction Industry

| # | Date Closed | Target | Acquirer | Classification |

|---|---|---|---|---|

| 1 | 08/14/2025 | AP Alternatives, LLC | STINorland USA, Inc. | Renewable Energy & Infrastructure |

| 2 | 08/06/2025 | Papich Construction Co., Inc. | Granite Construction Incorporated (NYSE:GVA) | General Contractors & Heavy Civil Construction |

| 3 | 08/04/2025 | H.W. Lochner, Inc. | Egis SA | Transportation Infrastructure & Consulting |

| 4 | 07/31/2025 | High Desert Aggregate & Paving, Inc. | Knife River Corporation (NYSE:KNF) | General Contractors & Heavy Civil Construction |

| 5 | 07/25/2025 | Dynamic Systems (DSI), LLC | Quanta Services, Inc. (NYSE:PWR) | Subcontractors & Specialty Trade |

| 6 | 07/22/2025 | Dawood Engineering | Woolpert, Inc. | Civil Engineering & Consulting |

| 7 | 07/21/2025 | CNA Consulting Engineers | Toltz, King, Duvall, Anderson, and Associates, Inc. | Civil Engineering & Consulting |

| 8 | 07/15/2025 | Progressive Services, Inc. | TopBuild Corp. (NYSE:BLD) | Subcontractors & Specialty Trade |

| 9 | 07/03/2025 | Independent Solutions, Inc. | Verdantas LLC | Civil Engineering & Consulting |

| 10 | 07/01/2025 | Pioneer Power, Inc. | Limbach Holdings, Inc. (NasdaqCM:LMB) | Subcontractors & Specialty Trade |

| 11 | 07/01/2025 | e3i Engineers, Inc. | Bowman Consulting Group Ltd. (NasdaqGM:BWMN) | Civil Engineering & Consulting |

| 12 | 06/30/2025 | CSRS, LLC | Westwood Professional Services, Inc. | Architecture & Engineering (A&E) |

| 13 | 06/25/2025 | DCCM, LLC | Court Square Capital Management, L.P. | Civil Engineering & Consulting |

| 14 | 06/19/2025 | Macadam Company, Inc. | Heartland Paving Partners LLC | General Contractors & Heavy Civil Construction |

| 15 | 05/31/2025 | Kraemer Trucking & Excavating, Inc. | Knife River Corporation (NYSE:KNF) | General Contractors & Heavy Civil Construction |

| 16 | 05/27/2025 | Rail Pros, Inc. | Littlejohn & Co., LLC | Transportation Infrastructure & Consulting |

| 17 | 05/15/2025 | Pavement Preservation Group, Inc. | The Sterling Group, L.P. | General Contractors & Heavy Civil Construction |

| 18 | 05/06/2025 | Poblocki Paving Corporation | Heartland Paving Partners LLC | General Contractors & Heavy Civil Construction |

| 19 | 05/01/2025 | PRI of East TN, Inc. | Construction Partners, Inc. (NasdaqGS:ROAD) | General Contractors & Heavy Civil Construction |

| 20 | 04/14/2025 | David Evans and Associates, Inc. | AtkinsRealis Group Inc. (TSX:ATRL) | Civil Engineering & Consulting |

| 21 | 04/10/2025 | Miller Land Surveying, Inc. | ZendaTech, INc. (NasdaqCM:ZENA) | Civil Engineering & Consulting |

| 22 | 04/08/2025 | Advanced Earth Sciences, Inc. | Verdantas, LLC | Civil Engineering & Consulting |

| 23 | 04/08/2025 | Horizons Engineering, Inc. | Verdantas, LLC | Civil Engineering & Consulting |

| 24 | 04/08/2025 | Atlantic Resource Consultants, LLC | Verdantas, LLC | Civil Engineering & Consulting |

| 25 | 04/08/2025 | Aqua Engineering, Inc. | Verdantas, LLC | Civil Engineering & Consulting |

| 26 | 04/08/2025 | Atlantic Environmental Consulting Services, LLC | Verdantas, LLC | Civil Engineering & Consulting |

| 27 | 04/03/2025 | Wallace Surveying Corporation | ZenaTech, Inc. (NasdaqGS:ROCK) | Civil Engineering & Consulting |

| 28 | 04/01/2025 | Fibrebond Corporation | Eaton Corporation plc (NYSE:ETN) | Manufacturing & Building Materials |

| 29 | 03/31/2025 | Talley Construction Company, Inc. | CRH Americas Materials, Inc. | General Contractors & Heavy Civil Construction |

| 30 | 03/04/2025 | XL Construction Corporation | Graham Group Ltd. | General Contractors & Heavy Civil Construction |

| 31 | 03/03/2025 | Punta Lima Wind Farm, LLC | Polaris Renewable Energy, Inc. (TSX:PIF) | Renewable Energy & Infrastructure |

| 32 | 02/11/2025 | Lane Supply, Inc. | Gibraltar Industries, Inc. (NasdaqGS:ROCK) | Manufacturing & Building Materials |

| 33 | 02/10/2025 | Green International Affiliates, Inc. | H.W. Lochner, Inc. | Transportation Infrastructure & Consulting |

| 34 | 02/03/2025 | Miller Electric Company, Inc. | EMCOR Group, Inc. (NYSE:EME) | Subcontractors & Specialty Trade |

| 35 | 02/03/2025 | Elcon Associates, Inc. | David Evans and Associates, Inc. | Civil Engineering & Consulting |

| 36 | 02/03/2025 | InSite Engineering, LLC | Godspeed Capital Management, LP | Civil Engineering & Consulting |

| 37 | 01/31/2025 | Alpha Inspections, Inc. | Wildan Engineering Inc. | Civil Engineering & Consulting |

| 38 | 01/14/2025 | KJM Land Surveying, LLC | ZenaTech, Inc. (NasdaqCM:ZENA) | Civil Engineering & Consulting |

| 39 | 01/13/2025 | Garden State Pavement Solutions, LLC | Heartland Paving Partners LLC | General Contractors & Heavy Civil Construction |

| 40 | 01/02/2025 | Overland Corporation | Construction Partners, Inc. | General Contractors & Heavy Civil Construction |

Let's Talk

Contact our Construction Industry Experts