Construction starts saw gains across the board in 2024 despite ongoing challenges to the sector. Moving forward, contractors are generally optimistic about the construction landscape; however, numerous potential headwinds remain, namely high interest rates, despite the fact that the Federal Reserve (“Fed”) cut rates three times in late 2024.

In addition, predictions run the gamut regarding the recent change in presidential administration. Some are optimistic that President Trump’s potential economic and tax actions could benefit construction firms. At the same time, Trump’s moves on immigration and tariffs could exacerbate challenges regarding the construction industry’s labor force and already-high material costs.

Recent Industry Performance

According to Dodge Construction Network (“Dodge”), during 2024, total construction starts rose 6.0% from 2023 to reach $1.15 trillion. Broken down further, residential starts grew 7.0% and nonresidential starts increased by 4.0%, while nonbuilding starts expanded by 7.0%.

Looking ahead, Richard Branch, chief economist at Dodge, indicates that market signs are positive, but interest rates remain high despite recent rate cuts by the Fed. High interest rates will likely remain a challenge to the U.S. construction market moving forward. Branch notes, “It’s probably going to take about 125, maybe even 150 basis points of cuts before we start seeing a more consistent growth in the economy and more consistent growth in the construction market.” Branch projects that, by mid-2025, the economy will start to see that movement.

As a result of these factors, in a November 2024 (latest available) forecast, Dodge forecasts that the total dollar value of U.S. construction starts will expand by 8.6% in 2025. Nonresidential starts are expected to increase by 5.9%, residential starts are projected to rise by 11.5% and nonbuilding starts will likely grow by 8.8%.

However, Branch indicates that Dodge’s outlook does not take the results of the 2024 presidential election into account. He says, “…the election of Donald Trump and the Republican majority in Congress could have a profound impact on the economy and on the construction sector in 2025. Further tax cuts aimed at small businesses could be a sizeable benefit to contractors and service providers and allow them to invest more in workers and equipment. Additionally, a reduction in red tape and looser regulatory policies may allow for construction projects to move more quickly through the planning stages to start.” At the same time, Branch notes that tariffs proposed by the incoming administration could become an issue for the construction industry since tariffs have the potential to increase material costs.

Nonresidential Construction

As mentioned previously, according to Dodge’s calculations, during 2024, U.S. nonresidential construction starts grew by 4.0% when compared to 2023, reaching $434.1 billion. More specifically, commercial starts rose 8.0%, institutional starts increased 16.0% and manufacturing starts declined 35.0%.

Meanwhile, project information firm ConstructConnect has a different take on nonresidential building starts in 2024. Overall, ConstructConnect indicates that nonresidential building starts totaled $377.4 billion in 2024, down 8.5% from 2023. Broken down further, ConstructConnect estimates that commercial starts saw a 4.8% increase, institutional starts rose by 7.2% and manufacturing starts fell by 51.3%. Further, ConstructConnect reports the following pattern for the commercial construction sector in 2024: hotel/motel, down 13.0%; retail/shopping, down 13.1%; retail miscellaneous, up 5.5%; parking garages, up 38.4%; amusement, up 43.6%; private office, up 7.4%; government office, up 9.6%; laboratory, up 18.0%; warehouse, down 13.9%; sports stadiums/convention centers, up 30.2%; and transportation terminals, up 9.6%. Within the institutional category, ConstructConnect states that specific segments saw the following pattern in 2024: religious, up 6.3%; hospital/clinic, up 42.6%; nursing/assisted living, down 19.4%; library/museum, down 1.4%; courthouses, down 3.1%; police stations and fire halls, up 19.4%; prisons, up 4.4%; military, down 45.5%; pre-school/elementary, up 10.7%; junior and senior high schools, up 13.6%; special and vocational schools, up 75.8%; colleges and universities, up 2.8%; and miscellaneous medical, down 7.1%.

Moving forward, according to Dodge’s November 2024 (latest available) forecast, nonresidential construction starts are projected to rise by 5.9% in 2025, spurred by growth in the retail, healthcare, and hotel segments. More specifically, Dodge anticipates that commercial construction starts will increase 7.0% in 2025. The retail segment will likely benefit from the recovery in the residential construction sector and resulting demand for new grocery stores and quick-service food outlets, while the hotel segment is expected to continue to benefit from positive travel trends. In addition, the warehouse segment should see growth as Amazon commences a new construction phase, albeit at a slower pace than in 2021 and 2022. Meanwhile, institutional construction starts are expected to rise by 4.0% in 2025, mainly due to the positive impact of strong residential construction as well as the fact that high interest rates generally do not impact the sector in the same way they affect the manufacturing and commercial sectors. Further, Dodge forecasts that manufacturing construction starts will grow by 9.0% in 2025. Despite mounting project delays—mainly due to slowing electric vehicle demand—and a lack of skilled labor, manufacturing starts are expected to benefit from growth trends in semiconductors, petrochemicals, and reshoring in 2025.

At the same time, according to ConstructConnect, total nonresidential building starts are projected to increase by 8.0% in 2025, with manufacturing starts up 19.0%, commercial starts up 7.0%, and institutional starts up 5.3%. Within the commercial segment, strong growth is anticipated for retail, hotels, and warehouses. Private and governmental offices are also expected to see growth in 2025, while sports stadiums and industrial laboratories will likely register declines. Meanwhile, in the institutional segment, ConstructConnect projects the largest gains in military structures and nursing homes, while prisons and religious structures are anticipated to see a drop.

Looking longer term, ConstructConnect forecasts that total nonresidential building starts will grow by 4.2% in 2026, 4.0% in 2027, and 4.2% in 2028.

Residential Construction

According to Dodge, residential construction starts expanded by 7.0% in 2024, reaching $389.2 billion. Specifically, single-family starts were up 15.0% year-over-year, while multifamily starts declined by 7.0%.

Meanwhile, the National Association of Home Builders (“NAHB”) reports that, during 2024, total housing starts reached 1.36 million, down 3.9% from 2023 when housing starts totaled 1.42 million. Broken down further, single-family starts were up 6.5% from 2023, while multifamily housing starts were down 25.0%. Moreover, the NAHB notes that, on a regional basis, total housing starts rose 9.1% year-over-year in the Northeast but fell 0.1% in the Midwest, 5.2% in the South, and 7.7% in the West.

Looking ahead, the NAHB projects that residential construction will register a decline of 0.5% in 2025, with single-family construction up an anticipated 1.4% and multifamily construction down an estimated 5.8%. “Uneven declines for mortgage interest rates in the coming quarters will improve housing demand but place stress on building lot supplies due to tight lending conditions for development and construction loans,” notes Danushka Nanayakkara-Skillington, group assistant vice president of forecasting and analysis at the NAHB.

Dodge is more optimistic than the NAHB in its November 2024 (latest available) outlook. The firm anticipates that residential construction starts will increase by 11.5% in 2025, with single-family starts up 9.0% and multifamily starts up 16.0%. Dodge’s Branch says that while multifamily starts were down in 2024, they will likely rebound in 2025 due to the fact that vacancy rates have increased over the past year. Branch notes, “This is still a fairly robust market.”

ConstructConnect concurs, forecasting 12.0% growth for the residential construction market in 2025, followed by growth of 13.8% in 2026, 12.1% in 2027, and 9.3% in 2028. During 2025, single-family and multifamily starts are expected to rise by 13.1% and 9.5%, respectively. However, the firm indicates that, even with anticipated growth, the multifamily segment will still lag its 2022 level.

With regard to the remodeling market, according to the Leading Indicator of Remodeling Activity (“LIRA”), published by the Remodeling Futures Program (“RFP”) at the Joint Center for Housing Studies of Harvard University (“Joint Center”), after two years of decline, spending on home improvements and repairs is forecast to expand by 1.2% in 2025. “A solid labor market, rising home values, and continued improvement in existing home sales are supporting greater activity in home remodeling and repair,” says Carlos Martín, director of the RFP at the Joint Center. “Upward trending retail sales of building materials and steady permitting for remodeling indicate that homeowners are slowly but surely expanding the pace and scope of projects compared to the last couple years.” Notably, the January 2025 LIRA report notes that the Joint Center has incorporated new benchmark data from the American Housing Survey, which resulted in a revision to the overall size of the remodeling market. According to Abbe Will, associate director of the RFP, “While expenditures are expected to grow only modestly this year, we’ve increased our projection for the remodeling market size in 2025 by $30 billion, or 6.4 percent, to $509 billion.”

Nonbuilding Construction

Nonbuilding construction starts grew by 7.0% in 2024 to reach a total of $324.3 billion, according to Dodge. Specifically, highway and bridge starts rose 6.0%; environmental public works starts gained 24.0% and miscellaneous nonbuilding starts increased 26.0%. Meanwhile, utility/gas plants starts fell 14.0%.

At the same time, ConstructConnect reports that heavy/civil engineering starts totaled $273.9 billion in 2024, up 12.1% from 2023, with specific segments seeing the following pattern: airport, up 62.0%; road/highway, up 5.4%; bridge, up 26.3%; dam/marine, down 1.3%; water/sewage, up 23.8%; electric power infrastructure, up 40.0%; and all other civil, down 20.4%.

Notably, on November 15, 2024, the White House reported that, since November 15, 2021, when the Infrastructure Investment and Jobs Act (“IIJA”) was signed into law, federal agencies announced approximately $568.0 billion in funding for more than 66,000 projects. This includes improvements on over 196,000 miles of roads; 11,400 bridge repair projects; replacement of 367,000 lead pipes; 580 port and waterway projects; over 400 airport terminal projects; over 2,400 drinking water and wastewater projects; and nearly 2,400 projects for water recycling, storage, conservation, desalination and other purposes. Further, over the three years since its implementation, projects related to the IIJA have created 940,000 construction jobs.

However, according to Engineering News-Record, some in the construction industry are concerned about whether President Trump will try to “claw back,” or rescind, enacted yet unspent funding from the IIJA and the Inflation Reduction Act (“IRA”). Brian Turmail, vice president of public affairs and workforce for Associated General Contractors of America, (“AGC”) says that a cut in the IIJA would be “exceedingly unlikely to happen,” especially in light of the broad bipartisan support for infrastructure. At the same time, though, in a speech in September 2024, Trump signaled that he would make an unspecified cut to the IRA. Turmail notes, “Clawing back the IRA funds would require some kind of repeal of the measure or portions of it. Politically that would be pretty challenging considering the wide geographic dispersal of the projects being funded.”

Moving forward, in its November 2024 (latest available) forecast, Dodge projects that total nonbuilding construction starts will grow 8.8% in 2025, mainly due to ongoing federal funding, which is slated to last through 2027. More specifically, Dodge expects to see the following pattern for specific nonbuilding segments in 2025: highways, up 14.2%; bridges, up 11.0%; other nonbuilding, up 4.1%; power plants/gas/communications, up 1.1%; and water supply systems, up 6.1%.

Meanwhile, the American Road and Transportation Builders Association (“ARTBA”) forecasts that highway construction will rise by 11.5% in 2025 after increasing by 7.1% in 2024. Bridge construction will likely expand by 8.9% in 2025, following 14.5% growth the previous year. According to Allison Black, senior vice president and chief economist at ARTBA, “Several states increased their own revenues to match federal funds and make additional transportation investments, using a combination of General Fund transfers, bond issues, business taxes and other user-fee increases.”

Further, ConstructConnect anticipates that heavy/civil engineering starts will increase by 5.3% in 2025, followed by growth of 6.0% in 2026, 4.8% in 2027 and 4.6% in 2028. The firm notes that, during 2025, heavy/civil engineering starts will “continue to exhibit growth but will not match the highs of the previous few years.” Miscellaneous civil engineering starts—including power projects, tunnels, and oil and gas projects—are projected to slow to 4.4% growth, compared to nearly 50.0% growth in 2024. At the same time, the roads, bridges and dams subsectors are all expected to see approximately 11.0% growth in 2025. The only subsector anticipated to see a decline in 2025 is airports.

Construction Industry Trends/Drivers

Construction Input Prices

The U.S. Bureau of Labor Statistics (“BLS”) reports that while construction input prices fell 0.2% in December 2024 when compared to November 2024, costs were up 0.9% year-over-year. Moreover, in December 2024, construction input prices were still 38.6% higher than in February 2020, prior to the onset of the COVID-19 pandemic. “Construction materials prices declined slightly in December and are virtually unchanged over the past two years,” notes Anirban Basu, chief economist of Associated Builders and Contractors (“ABC”). “Of course, there is significant variability across input categories. Much of the recent moderation can be tracked to lower energy prices; diesel prices, for instance, are down roughly $0.45/ gallon since December 2023. Prices for other inputs, like copper wire and cable or sand and gravel products, have escalated significantly over the past year. For the industry, however, the fact that overall input prices have remained flat in recent quarters is purely good news.” At the same time, though, Ken Simonson, chief economist at the AGC, indicates that, if the Trump administration imposes tariffs, material costs could increase. In an article published just before the presidential inauguration, Simonson said, “Costs are likely to rise much faster in 2025…construction materials are likely to experience sudden price increases if President-elect Trump follows through on his threats to impose steep tariffs.”

Labor Issues

Construction industry employment increased by 196,000 jobs, or 2.4%, in 2024, according to the BLS. However, ABC’s Basu notes that construction job growth slowed in recent months. According to Basu, “The 15,000 jobs added during the fourth quarter of 2024 represent the fewest over any three-month period since the middle of 2021.” Nonetheless, construction industry job growth was still significantly faster than hiring in the overall economy during 2024. At the same time, an AGC survey, released on January 8, 2025, found that 78.0% of contractors are having difficulties filling hourly craft positions, while 77.0% are finding it hard to fill salaried openings. Moreover, the three most frequently cited concerns of contractors surveyed by AGC were workforce related: rising direct labor costs (62.0% of respondents); insufficient supply of workers or subcontractors (59.0%); and worker quality (56.0%). In order to address labor challenges, construction firms are turning to technology, specifically artificial intelligence (44.0% of firms plan to invest in this technology in 2025); document management software (40.0%); accounting software (36.0%); and project management software (35.0%).

Construction Backlog

ABC reports that their “Construction Backlog Indicator,” which tracks commercial, institutional, heavy industrial and infrastructure construction, was at 8.3 months in December 2024, down from 8.4 months in November 2024 and down from 8.6 months from December 2023. Notably, backlog in the commercial and institutional category fell by almost one full month between December 2023 and December 2024 and currently stands at its lowest level since February 2023. Meanwhile, in the infrastructure category, during December 2024, backlog was at its highest level since August 2023.

Construction Confidence Index

All three metrics measured by ABC’s “Construction Confidence Index”— sales, profit margins and staffing—remained above 50.0 in December 2024, which indicates that contractors anticipate growth during the first six months of 2025. Moreover, the indices for sales and staffing were up in December 2024 when compared to November 2024. When comparing December 2024 to December 2023, all three indices saw increases. “While backlog inched lower in December, contractors broadly expect construction activity to pick up in the first half of this year,” says ABC’s Basu. “Contractor confidence remained extraordinarily elevated in December, with the share of contractors that expect their sales to increase over the next six months now at the highest level since early 2022. Despite that confidence, the path of interest rates will play a critical role in industry performance in 2025. If rates remain higher for longer, backlog may remain subdued, especially in the struggling commercial and institutional category.”

NAHB Builder Confidence Survey

Builder confidence increased slightly in January 2024 as contractors remained hopeful for economic growth and an improving regulatory environment, according to the NAHB/Wells Fargo Housing Market Index (“HMI”). Indeed, the HMI rose by one point to 47.0 in January 2025. (The HMI measures builder perceptions for the following six months on a scale of “good,” “fair” or “poor.” Any reading above 50.0 indicates that builders view the outlook as positive.) Moreover, two of the three indices of the HMI registered growth in January 2025; the index for current sales conditions was up three points to 51.0, while the index for traffic of prospective buyers increased two points to 33.0. However, the index gauging sales expectations over the next six months declined six points to 60.0, mainly due to elevated interest rates. “Builders are facing continued challenges for housing demand in the near-term, with mortgage rates up from near 6.1% in late September to above 6.9% today,” notes Carl Harris, chairman of the NAHB. “Land is expensive and financing for private builders remains costly. However, there is hope that policymakers are taking the impact of regulatory hurdles seriously and will make improvements in 2025.”

President Trump’s Executive Orders

On his first day in office, President Trump issued a series of executive orders, some of which could impact the construction industry, according to Construction Dive. During his inauguration address, Trump announced plans to resume construction of a border wall. In addition, by declaring a national energy emergency, Trump has directed federal agencies to eliminate delays in their permitting processes. At the same time, though, Trump’s declaration of a national emergency at the southern border may affect the availability of workers for U.S. construction projects. Moreover, as mentioned previously, impending tariffs could drive prices up on construction materials. While tariffs have not been imposed as of this writing, Trump announced on his inauguration day that his administration intends to impose 25.0% tariffs on Mexico and Canada as early as February 1, 2025.

Prairie’s 2024 Construction Survey

As part of Prairie’s 5th Annual Construction Survey, published in January 2025, survey respondents from construction companies with Employee Stock Ownership Plans (“ESOPs”) reported that backlog and profitability in 2024 were either similar to 2023 levels or better. At the same time, challenges included high materials costs and rising wages as well as finding qualified labor. Looking ahead, construction firms with ESOPs were optimistic when asked about their outlook for 2025 based on strong backlogs and the anticipation of further interest rate cuts. Moreover, many respondents are hopeful that the Trump administration will implement policies that will help the industry realize significant growth. In addition, leaders at construction firms with ESOPs are confident that their positive culture and hard-working employeeowners will help them navigate any challenges that may occur. Indeed, several survey respondents noted that employee-owners take more interest in all aspects of the business since they know that their choices may directly impact the ESOP share price. Others indicated that their employee-owners have helped with recruiting efforts in the midst of the labor shortage. For more information on trends in construction firms with ESOPs, see Prairie’s 5th Annual Construction Survey.

Read Prairie’s 5th Annual Construction Survey

Recent M&A Trends for the Construction Industry

Over the past several years, economic and geopolitical uncertainties have weighed on the global mergers and acquisitions (“M&A”) market, according to PwC. However, the firm believes that the global M&A market may be “back on an upward trajectory” in 2025, based on some recent dealmaking momentum, specifically at the top end of the market. Indeed, PwC reports that the volume of deals greater than $1.0 billion grew by 17.0% in 2024, while their average value also increased. At the same time, though, the volume of smaller and mid-sized deals declined by 18.0% in 2024. According to Brian Levy, global deals industries leader at PwC United States, “An M&A recovery is overdue, but it may struggle to maintain its recent momentum at a time when long-term interest rates are rising and valuations are high. It’s a market that will distinguish top dealmakers from the rest. To be successful, they will need deep industry expertise and a laser focus on value.”

With regard to activity in the construction and engineering sector, PwC reports that deal activity rebounded in late 2024 as a result of “increased confidence in a modest economic recovery, easing inflation and interest rate cuts.” Indeed, M&A activity in the construction and engineering sector was weaker in the first half of 2024 than it was in the second half.

Following are several notable transactions that took place in the construction and engineering industry at the end of 2024:

WSP Global Inc. (“WSP”) Acquires Power Engineers, Incorporated (“POWER”)

On October 1, 2024, global professional services firm WSP announced its acquisition of POWER, a U.S. engineering and environmental consulting firm in the power and energy sector, for US$1,780 million. “Today, we celebrate the start of an exciting new era for WSP and POWER as our teams join forces in creating the preeminent pure-play global consulting firm for the world’s energy transition. This milestone completes our strategic vision of expanding our capabilities in the Power & Energy sector by 2024 and unlocks a world of possibilities for our people, clients and communities,” notes Alexandre L’Heureux, president and CEO of WSP. “We are incredibly excited by the opportunities moving forward and can’t wait to start working together,” says Holger Peller, POWER’s president and COO. “Together, we’ll be able to offer our clients an even broader range of professional services thanks to our enhanced capabilities, and our teams will have opportunities to discover and contribute to a variety of amazing projects with colleagues from around the world.”

Parsons Corporation (“Parsons”) Acquires BCC Engineering, LLC (“BCC”)

On November 1, 2024, Parsons, a disruptive technology provider for the national security and global infrastructure markets, announced its acquisition of Florida-based BCC, a firm specializing in engineering services for transportation, civil and structural engineering projects across the Southeastern U.S., in an all-cash transaction valued at $230.0 million. According to Parsons, “The acquisition strengthens Parsons’ position as an infrastructure leader while expanding the company’s reach in the Southeastern United States, an area where the Infrastructure Investment and Jobs Act (IIJA) provided approximately $100 billion in Federal Highway Administration formula dollars for fiscal years 2022- 2026. The transaction is consistent with Parsons’ strategy of acquiring high-growth companies with greater than 10% revenue growth and adjusted EBITDA margins. BCC will be integrated into Parsons’ North America Infrastructure business unit.”

Construction Partners, Inc. (“CPI”) Acquires Lone Star Paving (“Lone Star”)

On November 4, 2024, vertically integrated civil infrastructure firm CPI, which operates in local markets across the Sunbelt, announced the acquisition of Lone Star, a central Texas-based vertically integrated asphalt manufacturing and paving company. According to Fred J. (Jule) Smith, III, CPI’s president and CEO, “This is an exciting day for CPI, and we are pleased to welcome the Lone Star team to the CPI family of companies. Lone Star is a uniquely complementary cultural fit within CPI, with its focus on operational excellence, employee advancement and smart vertical integration initiatives. The addition of Lone Star positions CPI to accelerate our ROAD-Map 2027 strategy and to deliver long-term value to our investors and other stakeholders.”

Looking ahead, PwC anticipates that the election of President Trump may lead to changes in the regulatory landscape and “drive investment focus toward different infrastructure opportunities.” Moreover, a number of construction and engineering subsectors, such as infrastructure, grid modernization and residential construction, will likely see sustained growth in 2025. Nonetheless, PwC anticipates that M&A activity in the nonresidential construction sector will remain subdued due to “continued challenges with high interest rates and margin compression resulting in a slower economic recovery in 2025.” However, some segments within the nonresidential sector—including data centers, lodging, healthcare and education—may see some deal activity during the year.

Data & Resources

Publicly-Traded Construction Companies

| ($ in millions) | LTM | LTM | Revenue Growth | Revenue Growth | LTM Margins | LTM Margins | EV / LTM | EV / LTM | EV / NFY | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Company | Stock Ticker | Country | Equity value | Enterprise Value | % of 52-Wk. High | Revenue | EBITDA | 1 Year | 3 Years | G. Profit | EBITDA | Revenue | EBITDA | EBITDA |

| Argan, Inc. | AGX | United States | $1,808 | $1,302 | 69.6% | $806 | $70 | 52.8% | 13.5% | 14.3% | 8.6% | 1.61x | 18.7x | 13.7x |

| Tutor Perini Corporation | TPC | United States | 1,274 | 1,686 | 70.3% | 4,281 | 16 | 13.7% | (10.0%) | 6.0% | 0.4% | 0.39x | n/a | 22.3x |

| Sterling Infrastructure, Inc. | STRL | United States | 4,334 | 4,023 | 68.5% | 2,103 | 324 | 8.7% | 17.1% | 19.6% | 15.4% | 1.91x | 12.4x | 12.7x |

| Comfort Systems USA, Inc. | FIX | United States | 15,128 | 14,781 | 77.1% | 6,517 | 779 | 31.2% | 22.2% | 20.4% | 12.0% | 2.27x | 19.0x | 17.7x |

| Construction Partners, Inc. | ROAD | United States | 4,437 | 4,876 | 76.5% | 1,824 | 212 | 16.7% | 26.0% | 14.2% | 11.6% | 2.67x | 23.0x | 13.5x |

| Dycom Industries, Inc. | DY | United States | 5,324 | 6,392 | 88.1% | 4,570 | 523 | 10.4% | 9.3% | 19.6% | 11.4% | 1.40x | 12.2x | 11.3x |

| EMCOR Group, Inc. | EME | United States | 20,214 | 19,186 | 80.6% | 14,235 | 1,375 | 17.7% | 12.7% | 18.4% | 9.7% | 1.35x | 13.9x | 13.4x |

| Fluor Corporation | FLR | United States | 8,250 | 6,450 | 80.0% | 15,875 | 303 | 3.3% | (0.7%) | 2.7% | 1.9% | 0.41x | 21.3x | 12.0x |

| Granite Construction Incorporated | GVA | United States | 3,800 | 3,985 | 82.6% | 3,964 | 261 | 17.8% | (0.5%) | 13.0% | 6.6% | 1.01x | 15.3x | 9.8x |

| Great Lakes Dredge & Dock Corporation | GLDD | United States | 739 | 1,141 | 85.2% | 742 | 126 | 33.7% | (7.0%) | 19.9% | 17.0% | 1.54x | 9.1x | 8.6x |

| IES Holdings, Inc. | IESC | United States | 4,312 | 4,227 | 67.3% | 2,884 | 337 | 21.3% | 23.4% | 24.2% | 11.7% | 1.47x | 12.5x | n/a |

| Limbach Holdings, Inc. | LMB | United States | 1,081 | 1,053 | 89.6% | 518 | 48 | 0.1% | (3.1%) | 25.9% | 9.3% | 2.03x | 21.8x | 17.4x |

| MasTec, Inc. | MTZ | United States | 10,877 | 13,038 | 83.6% | 12,180 | 919 | 3.9% | 23.8% | 12.8% | 7.5% | 1.07x | 14.2x | 13.2x |

| MYR Group Inc. | MYRG | United States | 2,282 | 2,371 | 78.2% | 3,537 | 120 | 0.9% | 17.5% | 8.5% | 3.4% | 0.67x | 19.8x | 21.8x |

| Orion Group Holdings, Inc. | ORN | United States | 310 | 357 | 65.8% | 781 | 30 | 10.6% | 0.1% | 10.7% | 3.9% | 0.46x | 11.8x | 8.6x |

| Primoris Services Corporation | PRIM | United States | 4,006 | 4,557 | 82.1% | 6,141 | 406 | 11.1% | 17.9% | 11.0% | 6.6% | 0.74x | 11.2x | 11.2x |

| Quanta Services, Inc. | PWR | United States | 43,959 | 47,901 | 81.4% | 22,903 | 1,916 | 17.4% | 23.1% | 14.1% | 8.4% | 2.09x | 25.0x | 21.1x |

| Aecon Group Inc. | TSX:ARE | Canada | 1,099 | 1,076 | 85.0% | 3,122 | 52 | (12.5%) | 7.1% | 7.3% | 1.7% | 0.34x | 20.5x | 17.3x |

| Bird Construction Inc. | TSX:BDT | Canada | 940 | 1,077 | 75.1% | 2,457 | 99 | 24.0% | 21.5% | 9.4% | 4.0% | 0.44x | 10.9x | 7.5x |

| Median | 80.0% | $3,537 | $261 | 13.7% | 13.5% | 14.1% | 8.4% | 1.35x | 14.7x | 13.3x | ||||

| Mean | 78.2% | $5,760 | $417 | 14.9% | 11.3% | 14.3% | 7.9% | 1.26x | 16.3x | 14.1x |

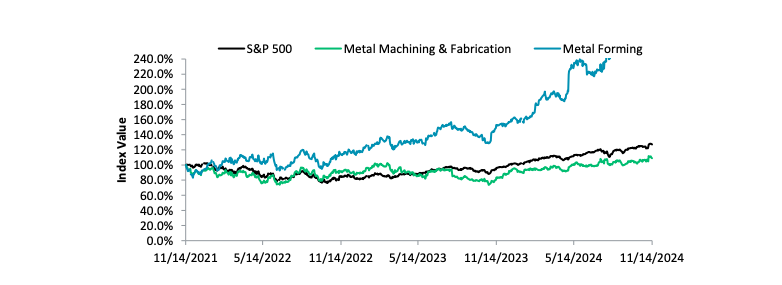

Construction Index Performance vs. S&P 500

Sources: S&P Capital IQ and public data

Since Q4 2020, the construction industry has outperformed the S&P 500, driven by strong infrastructure spending, rising demand for energy and telecom projects and robust backlogs. Favorable policies, strategic acquisitions and operational efficiencies have further fueled revenue growth and margin expansion.

Construction Industry Trends

Construction Starts

Source: Dodge Data & Analytics

Dodge Data & Analytics measures the seasonally-adjusted value of total U.S. construction starts each month, as well as the value of starts in nonresidential, residential and nonbuilding categories.

U.S. Construction Jobs

Source: Bureau of Labor Statistics

The Bureau of Labor Statistics releases job gains or losses in the industry and divides the figures into residential and nonresidential sectors.

U.S. Construction Spending

Source: U.S. Census Bureau

While often revised in subsequent months, construction spending figures each month from the U.S. Commerce Department examine the private and public construction sectors. Within the private sector, the report tracks single-family residential, multifamily residential and nonresidential starts.

Backlog Indicator

Source: Associated Builders and Contractors

The Associated Builders and Contractors’ backlog indicator is a forwardlooking economic metric that reflects the amount of work under contract that will be performed by commercial and industrial construction contractors in the months ahead.

Notable Closed M&A Transactions — Construction Industry

| # | Date Closed | Target | Acquirer | Classification |

|---|---|---|---|---|

| 1 | 1/13/2025 | Eberly & Associates Inc. | Pape-Dawson Engineers, Inc | Civil Engineering & Consulting |

| 2 | 1/8/2025 | Latite Roofing and Sheet Metal Company, Inc. | Sun Capital Partners, Inc. | Subcontractors & Specialty Trade |

| 3 | 1/3/2025 | Overland Corporation | Construction Partners, Inc. (NASDAQGS.ROAD) | General Contractors & Heavy Civil Construction |

| 4 | 1/1/2025 | CDI Engineering Solutions Inc | Tata Consulting Engineers Limited | Civil Engineering & Consulting |

| 5 | 1/1/2025 | LD Systems LP. | Clair Global Corporation | Industrial & Specialty Services |

| 6 | 12/23/2024 | Midwest Roofing Siding & Windows Inc. | RSS Roofing Services & Solutions LLC | Subcontractors & Specialty Trade |

| 7 | 12/17/2024 | United Engineers & Constructors, Inc. | Aecon Group Inc. (TSX:ARE) | Architecture & Engineering (A&E) |

| 8 | 12/16/2024 | BNP Associates, Inc. | Godspeed Capital Management LP | Transportation infrastructure & Consulting |

| 9 | 12/9/2024 | Kova Engineering Ltd | Industrial Inspection & Analysis, Inc. | Civil Engineering & Consulting |

| 10 | 12/4/2024 | Atlantic Southern Paving and Sealcoating LLC | Rose Paving LLC | General Contractors & Heavy Civil Construction |

| 11 | 12/3/2024 | Horvath Home Services Inc. | Punctual Pros | Building Systems & Home Services |

| 12 | 11/22/2024 | State Electric Corporation | E-J Electric Installation Co. Inc | Subcontractors & Specialty Trade |

| 13 | 11/18/2024 | The State Group, Inc. | Apollo Global Management Inc. (NYSE:APO) | Industrial & Specialty Services |

| 14 | 11/12/2024 | Meshek & Associates LLC | WSB & Associates Inc. | Civil Engineering & Consulting |

| 15 | 11/8/2024 | Stansbury Electric Co. | KSC Holdings, LLC | Subcontractors & Specialty Trade |

| 16 | 11/5/2024 | IME Experts-Consells | Akonovia Consultants Inc. | Civil Engineering & Consulting |

| 17 | 11/4/2024 | ArchKey Solutions LLC | 26North Partners LP | Subcontractors & Specialty Trade |

| 18 | 10/18/2024 | M G MC Laren, PC | KCI Technologies Inc. | Civil Engineering & Consulting |

| 19 | 10/16/2024 | Pinnacle MEP Holdings LLC | Blue Point Capital Partners LLC Blue Point Capital Partner | Subcontractors & Specialty Trade |

| 20 | 10/15/2024 | Freestate Electrical Construction Company | Sojitz Corporation of America | Subcontractors & Specialty Trade |

| 21 | 10/15/2024 | McKnight Construction Co Inc | Undivided Life LLC | General Contractors & Heavy Civil Construction |

| 22 | 10/1/2024 | POWER Engineers, Incorporated | WSP Global Inc. (TSX:WSP) | Architecture & Engineering (A&E) |

| 23 | 10/1/2024 | Stueve Construction LLC | Sound Growth Partners | General Contractors & Heavy Civil Construction |

| 24 | 9/26/2024 | Sargent Electric Company Inc. | Constructel Visabeira SA | Subcontractors & Specialty Trade |

| 25 | 9/13/2024 | American Residential Services LLC | Del-Air Heating Air Conditioning & Refrigeration Inc. | Building Systems & Home Services |

| 26 | 9/9/2024 | Bright Home Solar LLC | Civic Renewables Corp | Building Systems & Home Services |

| 27 | 9/9/2024 | Patriot Industries LLC | Rigid Constructors LLC | Manufacturing & Building Materials |

| 28 | 9/6/2024 | GRC Consulting Inc | Antimatter Construction Contractors | Civil Engineering & Consulting |

| 29 | 9/5/2024 | Proenergy Holding Company, Inc. | Energy Capital Partners, LLC | Renewable Energy & infrastructure |

| 30 | 9/5/2024 | Smith And Keene Electric Service Inc. | Cascade Residential Services LLC | Subcontractors & Specialty Trade |

| 31 | 9/4/2024 | Capital Elevator Co., Inc. | KONE Inc. | Transportation infrastructure & Consulting |

| 32 | 9/3/2024 | Johnson Engineering LLC | Apex Companies LLC | Civil Engineering & Consulting |

| 33 | 8/30/2024 | NRB Modular Solutions Inc. | ATCO Structures & Logistics Ltd. | Manufacturing & Building Materials |

| 34 | 8/21/2024 | Rommel Engineering & Construction Inc. | Lumin8 Transportation Technologies LLC | Subcontractors & Specialty Trade |

| 35 | 8/19/2024 | Superior Iron Works, Inc. | Extreme Steel Inc. | Subcontractors & Specialty Trade |

| 36 | 8/15/2024 | UGE International Ltd. | 1000896425 Ontario Ltd | Renewable Energy & infrastructure |

| 37 | 8/12/2024 | Quible & Associates PC | Withers & Ravenel, Inc. | Civil Engineering & Consulting |

| 38 | 8/5/2024 | TranSystems Corporation | Gannett Fleming Inc. | Architecture & Engineering (A&E) |

| 39 | 8/1/2024 | Jacob Bros Construction Inc. | Bird Construction Inc. (TSX:BOT) | General Contractors & Heavy Civil Construction |

Let's Talk

Contact our Construction Industry Experts