Overview

Sustainability is a concept that captures our ability to keep something going. In an ESOP company, the concept relates specifically to perpetuating the ESOP while maintaining the health of the business. This paper will discuss the elements that need to be examined when creating a strategy for a sustainable ESOP company. Furthermore, the tools and levers that can be utilized to optimize an ESOP company’s sustainability plan will be explored.

ESOP sustainability is not a new concept, but it has gained momentum in recent years. This trend has been driven by the following two factors. First, many ESOP companies are now mature—meaning most of the shares in the ESOP trust are allocated, and the company’s value may have also grown significantly since the initial transaction. Secondly, many companies are electing the 100% S corporation ESOP structure in order to recognize the associated tax benefits, and they desire to remain an ESOP in the long-term. For both of these reasons, there is a strong desire to develop a strategy that will allow a company to meet both its corporate goals and maintain the health of its ESOP as a benefit plan, cultural tool and value enhancer.

What is a Mature ESOP?

Let’s further explore the definition of a mature ESOP. The primary driver of whether an ESOP is mature is how much of the stock is allocated to participants. In the 80s and 90s, it was common for ESOPs to be implemented in phases. Typically, a 30% block of stock would be purchased first, and then ultimately over time, the ESOP would achieve 100% ownership of the company. This type of ownership transition often created a long, slow allocation of stock to participants (depending on how the transactions were structured). In recent years, it has become increasingly more common for the ESOP trust to buy 100% of the company’s stock in a single purchase to take advantage of the tax savings related to 100% S corporation ESOP structure. However, after 10 years, the ESOP plan must offer diversification rights to participants who are at least age 55, which can create sudden, unpredictable repurchase obligations (as participants can diversify up to 50% of their account balance over a six-year period). Even though the internal loan related to the purchase of 100% of the company’s stock can be amortized over a long period of time (typically 20 years), a significant portion of the shares will be allocated after 10 years.

Why Does the 100% S Corporation ESOP Structure Create a Desire for ESOP Sustainability?

Because the 100% S corporation ESOP has no federal tax liability, significant cash is generated for the company. This cash can be used to grow the business, as well as fund the repurchase obligation associated with sponsoring the ESOP. This structure is very attractive for a company to maintain in the long term because it provides a rich benefit for participants while still creating a healthy cash flow stream for the organization. So, in addition to the cultural elements that make employee ownership models so attractive, there are clear economic advantages to ESOP sustainability.

How Can a Company Begin to Create a Strategy for ESOP Sustainability?

The planning process for creating a sustainable ESOP company must begin with a high-level discussion to outline the long-term objectives of the company. The discussion should address business strategy, long-term growth objectives and benefit levels, with the goal being to align all of these considerations. During this process, trustees and managers should maintain integrated thinking and understand that it is a dynamic exercise that should be revisited periodically.

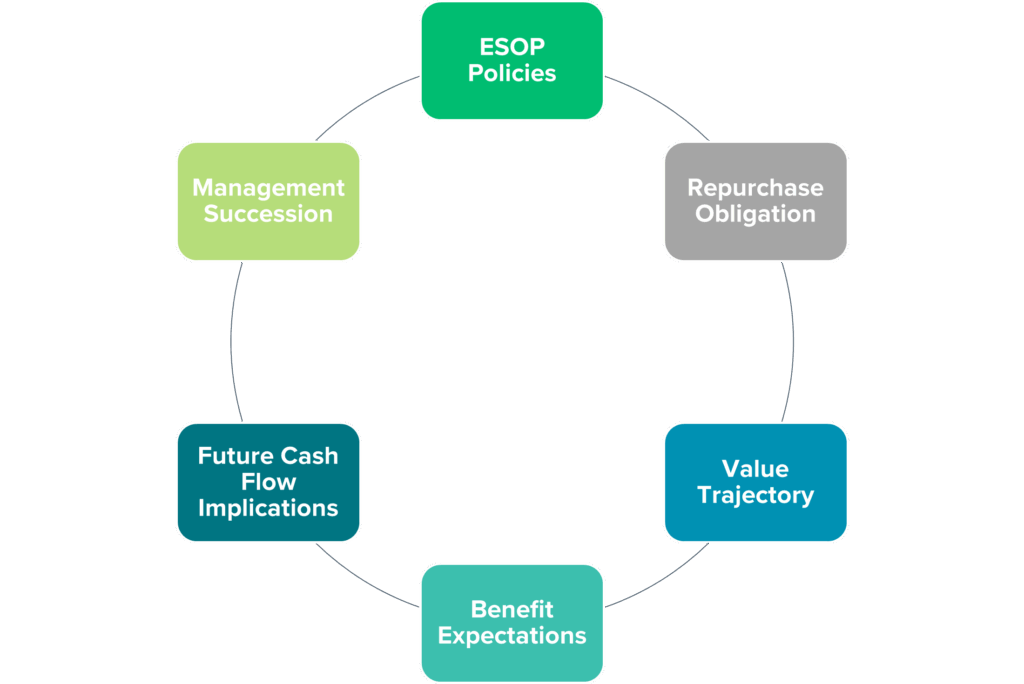

What variables does a company need to explore and address to develop a plan for the sustainable ESOP? Furthermore, what tools do companies have at their disposal for making changes? Certainly, the repurchase obligation, which is the company’s obligation to make a market for stock when that stock is to be bought back from ESOP participants, needs to be examined as the basis of any sustainability study. But to build a sustainable ESOP, the planning process must be more comprehensive than just a forecast of the shares that will become eligible for repurchase. The company must look not only at repurchase obligation, but at the interrelationship between repurchase obligation and valuation, the cash flow implications related to sponsoring the ESOP and how they affect other corporate objectives, and management succession. Based on its analysis of the foregoing, the company should understand how it can make decisions about ESOP policies, corporate governance and leadership development to influence a positive outcome.

Take Prairie’s ESOP Health Check

ESOP Sustainability Variables

Repurchase Obligation Planning

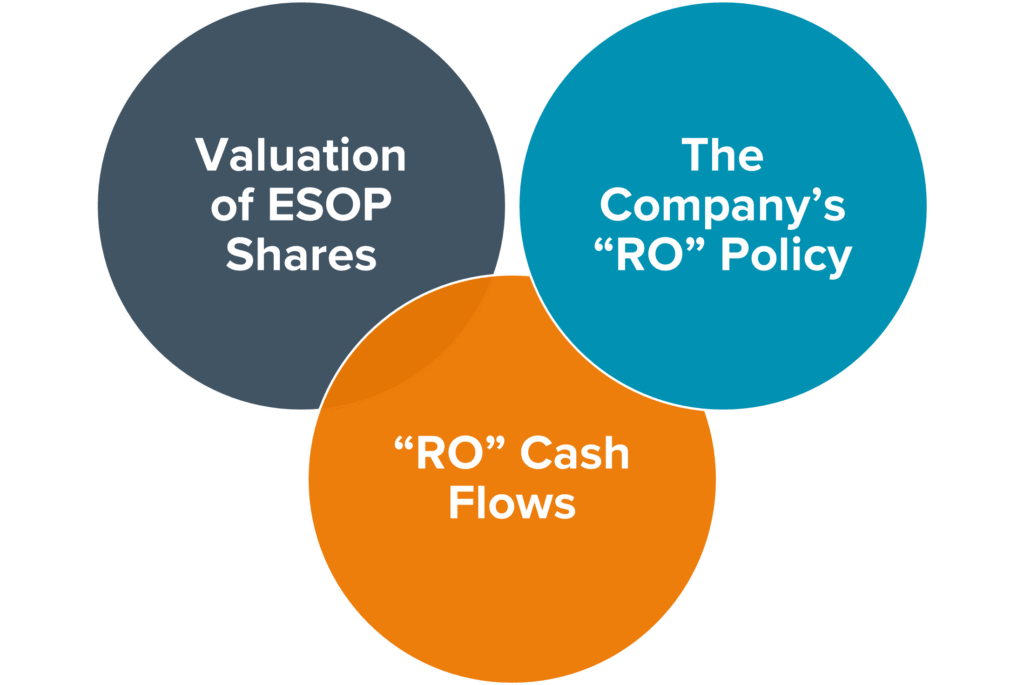

Repurchase obligation planning allows an ESOP company to quantify the number of shares that will need to be repurchased in order to fund the obligation that occurs when plan participants become eligible for distributions. The plan document dictates how the distributions are paid. In addition to correctly modeling the distribution rules, it is also important to understand the demographics and turnover patterns within the organization to create a reasonable forecast. Management should be intimately involved in the process, and it is important to project multiple scenarios to create a range within which the obligation will fall, as any single forecast will be wrong. Too often, the forecasting results that companies achieve are flawed because the planning is done in isolation, and assumptions regarding changes in share value over time are not tied to performance or value trajectory specifically. Therefore, it is important to expand the analysis to incorporate the interrelationship of the repurchase obligation and value trajectory to create more reasonable and reliable results.

The Interrelationship of the Repurchase Obligation and Share Value

A common mistake in the repurchase obligation planning process is that the share value trajectory driving the analysis is an afterthought or oversimplified. The missing element is the relationship that share value has with repurchase obligation and the simultaneous impact that a particular approach to dealing with repurchase obligation can have on value.

Inaccurate share price assumptions can cause the company to over or underfund the reserves it sets aside for future repurchase obligations, which can impact the financial health of the business. In order to plan effectively, an integrated approach, which involves reviewing the valuation methodology utilized by the independent appraiser, must be adopted. Debt repayment, benefit expenses, number of shares outstanding and funding methodology all need to be factored into the analysis, in addition to cash flows related to operating expenses and long-term business strategies. The planning process is iterative, dynamic and should involve the company’s professional advisors. Ultimately, the results of the analysis can then be used to help the company develop a policy for sustaining the ESOP, which then needs to be reflected in the appraiser’s calculation of value.

Integrated Approach To Repurchase Obligation

ESOP Policy Decisions

Policies that dictate how shares are repurchased, the structure and amortization of the internal loan between the company and the ESOP trust, where cash reserves intended to fund the repurchase obligation reside and the type of contributions made to the ESOP all have a significant impact on ESOP sustainability and the benefit provided by the ESOP. Too often, these policies are established when the plan is implemented and are forgotten until there is a problem. Unfortunately, the impact of these early decisions does not surface until the ESOP is mature, a time when any needed policy changes may be hard to change at make. Ideally, a company should create policies that are flexible, so that in the event changes need to be made, it is not impossible to do so.

There are multiple considerations that need to be reviewed when making decisions about the repurchase of shares. Not only does a company need to make decisions about the timing of the payments and whether or not they are paid in a lump sum or in installments, the repurchase method also needs to be determined. The repurchase method dictates whether shares are redeemed (distributed from the ESOP and retired to treasury) or recirculated in the ESOP trust (cash contributions are made to the trust to fund the repurchase of shares, which are then reallocated to active, eligible participants). Decisions about the timing and form of shares can be modified, but such changes typically require written policy changes, and cannot result in a cutback of benefits. Decisions about the method by which shares are repurchased can change each year, and a combination of methods can be chosen to target a specific benefit level.

The structure and amortization of the internal loan determine how rapidly shares will be allocated to participants and drive the benefit level that will be provided during the time that the loan is being repaid. Internal loans typically have longer amortization schedules but can be repaid more rapidly to provide a more targeted benefit level. Having a longer amortization schedule affords the flexibility to control the flow of shares more actively, whereas having a short schedule may be somewhat restrictive. Furthermore, once the term of an ESOP loan is set, it is very difficult to extend the term.

Cash Considerations

Regular cash contributions can be made to the trust, which are typically allocated pro rata to compensation. Or, S corporation earnings distributions or dividends can be paid to the trust, which are allocated pro rata to stock balance. The type of contribution made to the trust and the amount have different implications on how individual participant accounts grow over time. Regular contributions result in a broader allocation of stock, whereas S corporations earning distributions and dividends concentrate the benefit allocated to participants who hold more stock (which can compound over time, resulting in a have/have not dilemma).

The opposite of the have/have not dilemma that can occur is somewhat of a “Robin Hood” scenario. If a company becomes too focused on providing large benefits through the ESOP, it can be dilutive to shareholder value. This affects not only participants with large holdings in the ESOP, but also individuals who hold synthetic equity (which is typically distributed to retain talent, and influence performance, or can be attached to a transaction, such as a warrant). As a result, the individuals who are actually able to drive growth do not receive an appropriate return. In hindsight, these are easy outcomes to avoid, but they require planning.

If contributions made are in excess of what is required to amortize the ESOP loan or fund repurchase obligations, cash balances that are allocated to participant accounts will accumulate in the trust and become part of the benefit provided to participants through the ESOP. The assets are no longer available to the company for other uses. While the company may want to diversify the benefit provided through the ESOP, it is important to understand that once a participant terminates, the cash allocated to that individual is distributed to them, making this somewhat of an inefficient funding method.

It is also important to note that where the company sets aside cash reserves not only has a potential impact on benefit levels provided through the ESOP, but also creates a valuation difference. If the reserves are accumulated on the balance sheet, they remain an asset to the company and are reflected in value (even if earmarked for future repurchase obligations). Whatever strategy is adopted, it is important to involve the independent appraiser in your process and decision-making and to understand whether they are making specific adjustments for the reserves or the repurchase obligation.

Finally, management truly needs to understand how the ESOP, cash flow requirements and corporate decision-making interrelate. Developing an iterative planning process that not only forecasts the repurchase obligation, but also factors in the impact of debt, capital expenditures, profitability and tax liability under a range of financial assumptions empowers the company with a tool to make more informed, proactive business decisions.

Management Succession

Part of creating and ensuring a successful long-term operating model in any company is making sure that a clear management succession plan exists. This is especially important in an ESOP company, as the ESOP poses particular challenges to the organization that need to be well-understood. It is prudent, then, to develop a strategy for identifying and grooming future management so that leadership transitions are smooth, not disruptive. If no internal candidates exist, it may be necessary to look outside for successor management, which may pose additional challenges in an ESOP company. The benefit that the external hire might receive from the ESOP needs to be examined to determine whether it is market level for the position. If not, another method of awarding the candidate may need to be explored.

As part of planning for management succession, it is also important to determine whether or not the ESOP is the right ownership structure for the company in the long term. If not, this planning process allows the company a longer planning horizon to prepare itself for sale.

Summary

To properly plan for and develop a strategy to create a sustainable ESOP, an ESOP company has to explore many different variables in an iterative fashion under multiple scenarios. The exercise includes not only quantitative analysis related to forecasting the repurchase obligation and financial modeling, but also an exploration of the various tools that an ESOP company has at its disposal to make changes to its existing policies. Among all the things that a company plans for on both strategic and operating fronts, it is quite likely that ESOP sustainability will have the longest horizon. Some of the levers that are used to impact an ESOP’s financial “behavior” can take a long time to reveal their consequences, so planners need to get comfortable with a very different kind of analysis. ESOP Trustees and management need to understand how the ESOP impacts their business in the short and long term, and developing a plan for the sustainable ESOP allows them to do so while enabling confident decision-making.

Franco Silva is a Director at Prairie Capital Advisors, Inc. He can be contacted at 312.445.9213 or by email fsilva@prairiecap.com.