Executive Summary and Key Points

Prairie’s 6th Annual ESOP Construction Survey (“Prairie Survey”), which polled leaders at construction companies with Employee Stock Ownership Plans (“ESOPs”) in November 2025, illustrates an industry that remains resilient despite continued macroeconomic headwinds and uncertainty. While higher interest rates, labor scarcity and rising competitive pressure continue to influence project flow, most ESOP-owned construction firms report stable backlogs and healthy demand heading into 2026. Several companies even described record performance, citing organizational discipline and the cultural advantages of employee ownership as key drivers of consistency in a volatile market. In addition, continued strength in data center and infrastructure-related projects supported record backlogs and operating performance.

Looking ahead, ESOP firms are sharpening their focus on workforce depth, technology adoption and strategic growth. Companies expect 2026 conditions to resemble 2025 unless interest rates decline further—which many believe would unlock delayed projects and accelerate bidding activity. Technology continues to gain traction across the industry, particularly artificial intelligence (“AI”)-enabled tools that improve decision-making, project planning and estimating. At the same time, firms are planning for longer-term ESOP sustainability and investing in leadership development to successfully transition management teams.

- Market resilience continues, with stable backlogs and strong demand, supported in part by data center and infrastructure-related work, despite pressure from interest rates, labor scarcity and competitive bidding.

- Workforce depth remains the top constraint, with firms seeking experienced tradespeople, supervisors and office leadership to enable growth.

- Technology adoption, especially AI, is accelerating, influencing estimating, scheduling, job costing and decision-making across the industry.

- Employee ownership strengthens culture, supporting accountability, retention and responsiveness, particularly among long-tenured employees.

- ESOP sustainability planning is rising in priority, with firms conducting repurchase liability studies and building governance discipline.

- Leadership development is a strategic focus, as companies invest in mentoring, succession planning and talent development to drive future growth.

Industry Trends

According to Dodge Construction Network (“Dodge”), on a year-to-date basis through October 2025 (latest available), total construction starts increased 5.9% year-over-year, driven by a 5.6% rise in nonresidential activity and a 19.8% gain in nonbuilding starts, partially offset by a 5.1% decline in residential construction. Furthermore, for the 12 months ending October 2025, total construction starts rose 8.1% compared with the prior 12-month period, supported by a 7.5% increase in nonresidential activity and a 22.9% gain in nonbuilding starts, while residential starts declined 3.1%.

Looking at 2025 overall, in a September 2025 (latest available) outlook, Dodge projects that U.S. construction starts will total $1.21 trillion, up 3.2% from 2024, supported by data center and infrastructure construction projects. However, total building construction (which excludes nonbuilding sectors) is expected to decline by 2.0% in square footage during 2025. Dodge attributes this weakness to rising uncertainty for both businesses and consumers stemming from “rapid changes to economic and fiscal policies.”

Engineering News-Record reports that the construction industry in 2025 was supported by strong demand for megaprojects, particularly data centers, but faced meaningful headwinds as labor shortages, elevated costs and tariff-related trade uncertainty weighed on broader activity. These pressures stemmed from tight labor markets, shifting federal trade and tax policies, and hesitation among owners and manufacturers to commit to large projects amid uncertainty around the durability of current incentives. As a result, while large-scale projects helped support backlogs and spending, uneven sector performance kept overall growth muted and outlooks cautious heading into 2026.

For 2026, Dodge forecasts that total construction will expand 4.0% to reach $1.26 trillion, with nonresidential starts up an estimated 3.0% to $481.0 billion, residential starts up approximately 6.0% to $418.0 billion and nonbuilding starts up an estimated 4.0% to $361.0 billion.

Current Business Conditions

The Prairie Survey found that, across the ESOP construction landscape, the market remains active but uneven as interest rates, competition and labor dynamics continue to shape performance. Several survey respondents pointed directly to financing pressures, with the CFO of a new home construction company noting that “interest rates are affecting profitability,” while the President of a heavy construction company shared that, “everything remains on target…business is stable and should improve as interest rates drop.” Additionally, competitive intensity is increasing, especially in bidding environments, where the President and CEO of a specialty trade contractor company stated, “We are having a good year, but the plan and spec market is getting very competitive.”

Conditions vary by region and sector, yet many companies describe strong activity despite persistent challenges. As the CFO of an electrical contractor noted, “We work almost exclusively in the West Michigan market…demand remains strong despite pressure for labor,” while the President of another electrical contractor emphasized labor concerns more bluntly: “Our biggest headwind is qualified skilled labor.” Moreover, tariff impacts range widely, with the President of a heavy highway construction firm commenting that “tariffs have had no real effect,” and the President of a full-service general contracting company observing that “tariffs have affected customers from moving forward with projects.”

“We are having another record year and would look for the same in 2026.”

CFO of an electrical contractor

Technology’s Impact on the Construction Industry

Technology is influencing nearly every aspect of ESOP construction firms’ operations, and Prairie Survey respondents described how new tools are beginning to shape everything from decision-making to on-site efficiency. Several leaders emphasized that adoption is accelerating, with the CFO of a custom home builder noting that “we will be increasing our use of technology to improve decision making and speed of information gathering” and the President and CEO of a mechanical contractor observing that “AI is starting to infiltrate throughout our organization.” At the same time, a portion of respondents voiced caution about the pace and implications of technological change. Some expressed skepticism, including the President of a customized garage and shed construction company who noted being “very skeptical of AI” and going on to say that “thinking and learning is being replaced with AI.” Others pointed out that the industry has yet to see meaningful effects, with the CEO of a full-service construction company describing the impact as “too soon to see” while still projecting that “it will be big.”

“We’ve been improving processes but are in the middle of planning for how AI and other forms of technology can be used in the upcoming 12 months. (It will change between now and then anyway, so can’t look out any farther than that).”

CFO of a full-service electrical contractor

The ESOP’s Impact and Educating Employee-Owners

According to Certified EO, an organization that is building a network to bring national recognition to employee ownership through the use of a marketing and certification program, ESOP adoption within the construction industry is concentrated across several major subsectors, led by commercial construction with 193 firms, followed by specialty trade contractors with 139 firms, heavy and civil engineering construction with 123 firms, electrical contractors with 119 firms, and plumbing and HVAC contractors with 88 firms. In broader context, the National Center for Employee Ownership reports that there are 6,548 ESOPs in the U.S., of which approximately 16.0% operate within the construction industry.

Sources: Certified EO and National Center for Employee Ownership

Leaders at construction companies with ESOPs consistently described employee ownership as a meaningful cultural anchor that strengthens engagement and reduces turnover. One anonymous respondent to the Prairie Survey noted that even in competitive labor markets, the ESOP has become “a great [retention] and hiring tool,” helping employees think more long-term about their future with the company rather than chasing wage increases elsewhere. Others emphasized its cultural influence, with the President and CEO of a mechanical contractor saying their ESOP “has been the reason for our significant growth and profitability.” A trend emerged with multiple respondents noting that the ESOP held a strong impact on tenured employees, but struggled to hold much value with newer employees, with the CFO of a heavy civil contracting company noting, “We still struggle with new employees in the 0-3 years [range].”

Beyond cultural effects, ESOP leaders also pointed to tangible operational benefits in 2025, particularly in how employee-owners helped companies navigate day-to-day challenges. Many respondents pointed to the advantage of having frontline employees who understand the work intimately, with the President and CEO of a mechanical contractor noting that employee-owners “are on the front line and see what changes need to be made.” Others highlighted the operational lift created by an ownership mindset, with the President of a heavy civil construction company sharing that employee-owners “have continued to improve production and quality,” and the CFO of an electrical contractor noting that they are “ready to step in and support the situation even outside their responsibilities.”

As employee ownership has become more embedded in construction firms, many leaders reported a layered approach of combining structured financial literacy programs, ESOP committees, open-book management practices and ongoing internal communication when asked how they educate employee-owners on the value and function of their ESOP. Still, several respondents acknowledged that education remains a work in progress, with the CFO of a residential new home and custom builder noting, “We have not done a great job on education during our first year as an ESOP. This needs to be a focus in 2026.” Others emphasized the unique challenges faced by newer plans, including the President of a specialty trade contractor who shared, “We are a very young ESOP…To this point, we have only provided some high-level explanations with some slides. We look to form an ESOP Committee in the near future and ramp up communication when first statements are delivered in the next 5 or 6 months.” More mature ESOPs highlighted the value of consistent, branded internal outreach, such as the CFO of a full-service heavy civil infrastructure contractor whose marketing team “does educational ESOP videos and updates throughout the year, especially during Employee Ownership Month in October and during Shareholder Week,” underscoring how intentional communication can strengthen employee-owner engagement over time.

“Over the years, we have seen positive impacts from our ESOP, driving Company culture, an owner’s sense of urgency and our employees thinking and behaving more like an owner. Employee retention has also been positively impacted for employees who stay with the Company for a period longer than 5 years.”

CFO of a specialty trade contractor

ESOP Sustainability

In response to the Prairie Survey, construction company leaders described a wide range of experiences with ESOP sustainability studies, with many noting that these evaluations helped them better understand long-term repurchase obligation and strengthen governance practices. Several respondents emphasized that their companies are still early in the process, with more than one reporting that they were conducting a study at the time of the survey. The CFO of a general contractor specializing in horizontal construction shared that they did their “first study in 2025. It helped us articulate what we already knew about our ESOP obligations. It was great to see our thoughts validated. We will likely do it again every 2-3 years.”

Looking ahead, companies expressed varying levels of preparedness and intent regarding future sustainability planning, with some already committed to near-term studies and others taking a longer runway based on ESOP maturity. Several leaders indicated they plan to move forward soon, including the CFO of a specialty trade contractor who noted, “I’m trying to get one done within the next 6 months.” Others are relying on internal tools for now. As the CFO of a luxury custom home builder respondent explained, “We have developed an internal study for the time being and will look at a more formal one down the road.” Meanwhile, younger ESOPs emphasized that they are still building foundational elements before pursuing a full sustainability study, with the President of a heavy civil engineering and general construction firm leader sharing, “We are a young ESOP still working toward meeting feasibility study goals…likely 5 years or more from a sustainability study.”

“We’ve had one study in the past, currently working on the second. It’s very beneficial in that it helps you realize how much funds need to be set aside annually to be able to meet the buy out obligations.”

Vice President of a multi-trade commercial contractor

Next Generation Leadership

Many leaders at construction companies with ESOPs emphasized the importance of developing strong internal leadership pipelines, though their success levels varied widely. As part of the Prairie Survey, several respondents described strong internal pipelines, with the President of a specialty trade contractor noting that their organization has been “very intentional in this area over the past 5 years and [has] built a solid bench of leaders for moving forward.” Others spoke of previous success with leadership training: “There has been succession planning for years, which some came to fruition in late 2024. We continue to plan for the next group of leaders as well. We use peer groups, leadership training, and mentoring.” At the same time, several companies acknowledged that leadership development remains a work in progress, with some candidly noting gaps they are actively working to close. The COO of a commercial construction contractor shared, “We have fallen short, but we just hired a Talent Development Director who will be focused on succession planning,” underscoring a growing commitment to formalizing the process. Others pointed to meaningful early progress, including a leader who reported, “We are getting better. We completed our first-year mentoring/leadership program and have identified areas for improvement.”

“We have key players in place, and we still have more to do. The ESOP has created a collaborative culture between the field and management that helps to build on trust and succession. I don’t think we ever stop developing leaders.”

CFO of a heavy civil contractor

Outlook for 2026

When asked what single change would most strengthen their market position in 2026, the Prairie Survey respondents pointed to a mix of financial, workforce and strategic priorities. Many respondents emphasized that interest rates continue to shape project activity, with one leader at a general contractor calling for the “Fed [to] drop interest rates to align with market demand.” A majority of respondents identified internal capacity as their greatest opportunity for improvement, with the CFO of an electrical contractor remarking that they would “hire additional experienced electricians that fit our culture,” underscoring how labor availability remains a defining factor in operational momentum. Additionally, several leaders identified strategic expansion as key to strengthening their competitive position. The President of a heavy highway construction firm highlighted plans for “expansion into other markets in the [South],” while multiple others referenced deepening their private-sector presence or enhancing marketing focus.

Respondents expressed a balanced outlook for 2026, with many anticipating continued strength while others expect a year that closely mirrors 2025. Several leaders pointed to macroeconomic factors as a potential tailwind, including the President and CEO of a mechanical contractor who noted that “lower interest rates will propel the economy forward for the next couple of years.” Others conveyed enthusiasm about sector-specific drivers. The President of a specialty trade contractor predicted that “the remodeling and construction industry will experience growth soon.” However, a meaningful portion of respondents foresee relatively flat conditions, expecting 2026 to be stable but not markedly different from the current environment. Some anticipate that 2026 will be consistent with an already solid 2025, supported by steady backlogs, predictable demand and ongoing data center activity. The CFO of a luxury custom home builder observed, “Our current outlook is similar to current and past years. Backlog remains steady; market remains steady.”

“Our outlook is positive. We hope to repeat our 2025 results in 2026. The challenge is tighter margins and bettering our original estimated markup during construction.”

President of a heavy construction firm

Building on those expectations for 2026, respondents also acknowledged several wildcard factors that could shift their outlook, both positively and negatively. Many centered on macroeconomic variables, with multiple respondents citing interest rates as the biggest unknown and the Vice President at a multi-trade construction and service firm noting that “materials pricing and availability” could significantly influence performance. Others pointed to tariff policy or political developments outside their control, including concerns that “politics in general is a wildcard” that affects funding and project flow, according to the CEO of a general contractor. Several respondents referenced risks tied to specific markets, from potential pullbacks in data center activity to the possibility of recessionary pressures.

“Tariffs and/or retaliatory VAT taxes on materials will cause material costs to be a major concern/avenue for error when estimating and bidding new work with potential start dates well into the future.”

CFO of a commercial contractor

“Finding good people both in the field and the office continues to be a significant focus for us. It is getting better than in years past, but our growth continues to be hampered by a workforce shortage”

President and CEO of an electrical contractor

Emerging Trends Through 2030

When asked to identify emerging trends and innovations that will likely shape the construction industry by 2030, Prairie Survey respondents overwhelmingly cited technology, especially AI, as the most transformative force. Many see AI driving efficiency and accelerating decision-making, with one leader at a general contractor noting that “AI will have an impact on the pre-construction process management of construction projects” and the President of a civil infrastructure contractor emphasizing the growing role of “technology, including AI and autonomous machines.” Others, however, shared concerns over the limitations of AI, with the President of a concrete construction company noting, “AI might enter into estimating, but I’m not clear on how it could assess the many factors when compiling a bid. It could do quantity takeoffs, but accurate pricing would be a stretch.”

Beyond AI, several respondents highlighted structural and industry-wide shifts. Some pointed to consolidation as private equity activity increases, while others anticipate greater use of prefabrication, hybrid and electric vehicles, or innovations that make construction “more productive and build faster with less people,” as highlighted by the CEO of a general contractor.

“I truly believe we are going to have to find a way to make construction more productive and build faster with less people.”

CEO of a general contractor

Closing Statement

Taken together, Prairie’s 6th Annual ESOP Construction Survey reflects an industry operating with greater consistency amid ongoing uncertainty. While hesitation around interest rates, labor availability and policy continues to shape decision-making, ESOP-owned construction firms are largely maintaining solid backlogs and consistent operating results, supported by continued demand for data center, infrastructure and other nonbuilding projects. At the same time, respondents are increasingly focused on strengthening their organizations from within, with greater attention to leadership development, technology adoption and ESOP sustainability to support long-term continuity. This year’s responses reflect a balanced, forward-looking approach, with firms positioning themselves to deliver durable performance through 2026 and beyond despite uneven macroeconomic conditions.

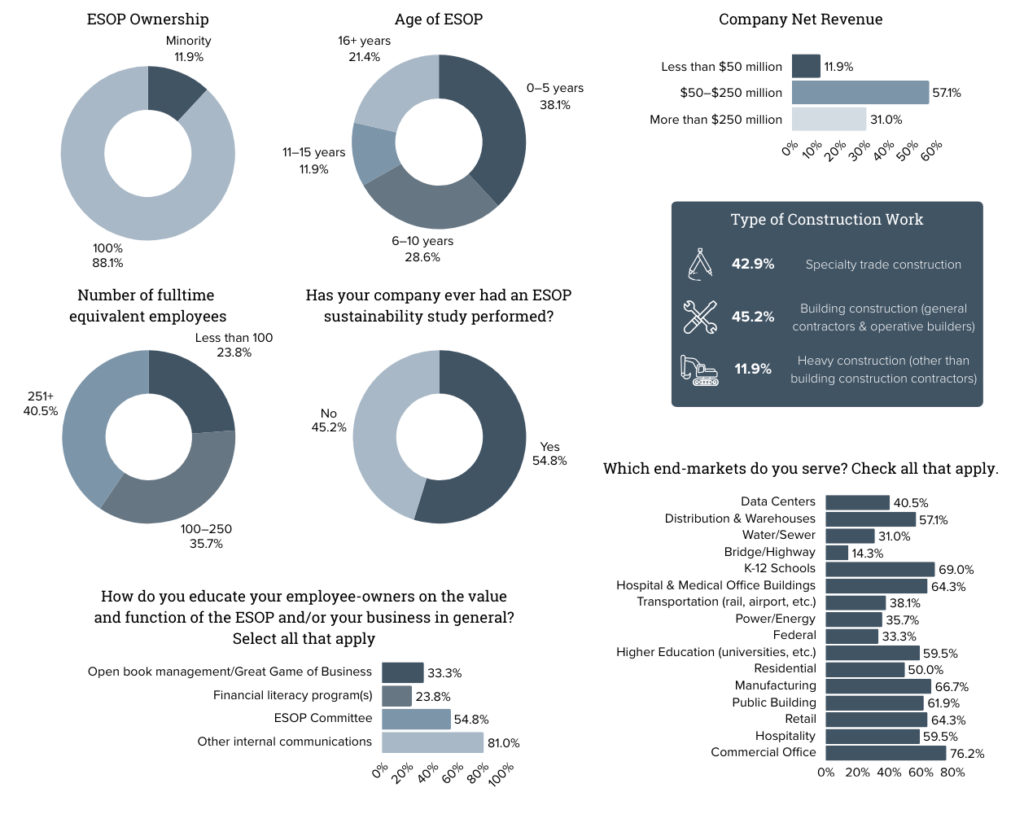

Demographics & ESOP Related Questions