The architecture and engineering industry entered 2026 facing a market defined by uneven but resilient growth. While overall construction activity continued to expand through 2025 and into early 2026, demand has become increasingly concentrated in high-growth areas such as data centers, artificial intelligence (“AI”) infrastructure, power and water projects. At the same time, more traditional sectors, including office, retail and manufacturing construction, remain under pressure from elevated interest rates, economic uncertainty and shifting development priorities. Even amid these mixed conditions, many of the industry’s largest engineering firms reported strong revenue growth, expanding backlogs and solid profitability driven by infrastructure and technology-related demand.

Looking ahead, the industry continues to balance long-term opportunity with ongoing uncertainty. Investment tied to the Infrastructure Investment and Jobs Act (“IIJA”) and the rapid expansion of AI-related infrastructure is expected to support activity across several end markets, while labor shortages, tariff uncertainty and slower design contract activity continue to weigh on broader growth expectations. In response, firms are increasingly investing in AI and digital tools to improve efficiency and strengthen their competitive positioning, while elevated mergers and acquisitions (“M&A”) activity reflects continued confidence in the sector’s long-term outlook.

Recent Industry Performance

In 2025, total U.S. construction starts grew by 5.4% compared to 2024 to reach $1.24 trillion, according to Dodge Construction Network (“Dodge”). Specifically, nonresidential construction increased 5.4% to $473.0 billion, residential construction decreased 4.8% to $374.0 billion and nonbuilding construction starts increased 18.7% to $396.0 billion. Further, during the first three months of 2026 (latest available), total construction starts rose by 12.8% compared to the same period in 2025. Nonresidential starts were up 6.3%, residential starts grew 2.6% and nonbuilding starts expanded 37.9%. “A few strong categories overcame slight weakness in all the others in March [2026],” stated Eric Gaus, chief economist at Dodge. “The commercial segment shows the most strength with 12 month growth for all subcategories except warehousing.”

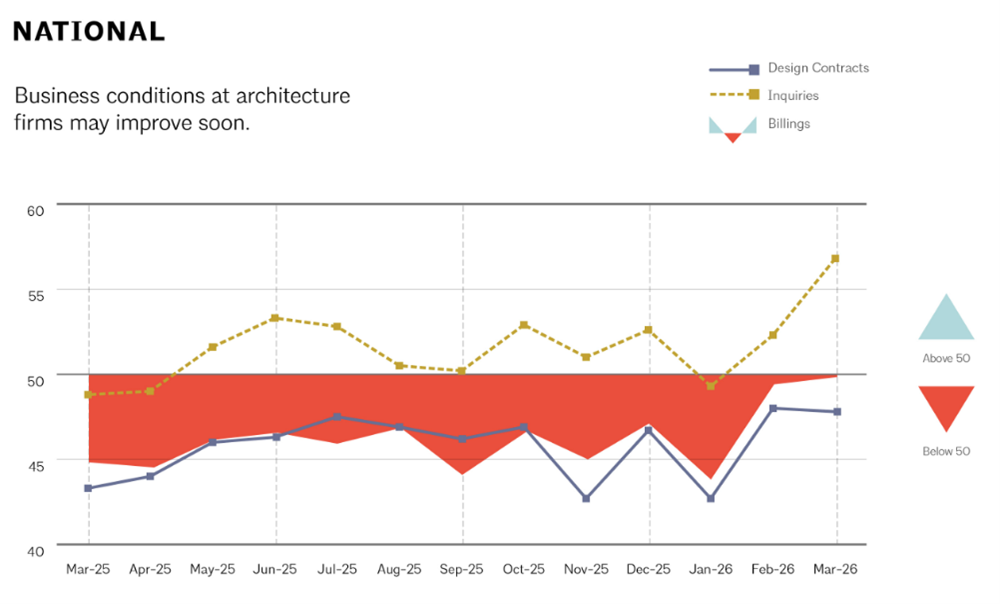

Additionally, the American Institute of Architects (“AIA”)/Deltek Architecture Billings Index (“ABI”) registered a score of 49.8 in March 2026 (latest available), indicating that firm billings were essentially flat, with the share of firms reporting increases roughly equal to those reporting declines. (The ABI, published monthly by the AIA, is a leading indicator of nonresidential construction activity: a score of 50.0 indicates no change in billings, readings above 50.0 indicate growth and readings below 50.0 indicate contraction.) This marks the closest the index has come to the 50.0 threshold since the first quarter of 2023. Recent data suggests some improvement in activity, as inquiries into new projects increased in March 2026 and firm backlogs rose to an average of 6.6 months, the highest level since December 2023. However, the value of newly signed design contracts declined for the 25th consecutive month in March, with the pace of decline accelerating from February 2026. Earlier in the year, ABI readings remained below 50.0, registering 43.8 in January and 49.4 in February, reflecting continued softness in conditions, although trends appeared to be approaching stabilization.

Major engineering and infrastructure consulting firms reported continued revenue growth, expanding backlogs and solid profitability through 2025 and into early 2026, supported by strong demand across infrastructure, power, water and technology-related projects. Several firms also noted growing activity tied to data centers and AI-related infrastructure, while recurring and compliance-driven service lines continued to provide stability despite ongoing economic uncertainty.

Outlook for 2026

According to the AIA Consensus Construction Forecast Panel (“Panel”), nonresidential building construction is expected to grow modestly through 2027, reflecting continued economic uncertainty and uneven performance across sectors. The Panel projects spending on building construction to increase just 1.0% in 2026 and 2.2% in 2027, levels that are not expected to keep pace with rising construction costs. Within major categories, commercial construction spending is projected to grow 3.0% in 2026 and 3.5% in 2027, while institutional construction is expected to increase 2.7% and 2.8%, respectively. In contrast, manufacturing construction spending is forecast to decline 3.9% in 2026 and an additional 0.9% in 2027.

The Panel’s outlook reflects a market characterized by imbalance, with strong growth concentrated in select areas such as data centers, while more traditional segments, including offices and retail facilities, face stagnation or decline. Data center construction is expected to continue expanding, with spending projected to increase by 26.0% in 2026 and nearly 17.0% in 2027, while office construction is anticipated to decline at a “double-digit rate” over the same period.

Further, the AIA attributes these trends to a combination of structural and macroeconomic factors, including uncertainty around tariff policy, labor availability, high interest rates and reductions in federal spending. Tariff uncertainty in particular has made long-term planning more difficult for developers, as shifting policies affect supply chains and investment decisions. At the same time, labor constraints remain significant, with foreign-born workers accounting for approximately one-quarter of the construction workforce and a higher share of the craft workforce, many of whom are vulnerable to immigration enforcement.

Additionally, leading indicators suggest limited near-term improvement, as architecture billings and design contracts have remained weak, indicating that new project activity has not yet shown signs of a significant recovery. The AIA notes that while construction starts showed some growth through the first 11 months of 2025, increased project delays and cancellations have raised concerns about the timing and realization of future spending. As a result, the nonresidential construction market is expected to remain constrained, with growth prospects varying widely across individual sectors.

While construction indicators point to constrained growth, engineering firm sentiment reflects a more balanced outlook. The American Council of Engineering Companies Research Institute’s most recent “Engineering Business Sentiment” study, conducted in January 2026, indicates that future sentiment remains positive across key measures, though more measured than in prior periods. Firms’ outlook for their own financial performance is the strongest indicator, with a net rating of +36, followed by industry sentiment at +14, while expectations for the U.S. economy have returned to slightly positive territory at +3. By sector, future industry sentiment is highest in the data centers and energy and utilities segments (+89 net rating), while several other sectors remain below year-over-year levels. In addition, 46.0% of engineering firms anticipate an increase in project backlog in 2026, resulting in a net rating of +31. At the same time, the top concerns among engineering companies include political instability and uncertainty, broader economic uncertainty, and ongoing pressures related to inflation and tariffs, although concern surrounding these factors has moderated compared to prior periods.

Architecture and Engineering Industry Trends

- IIJA Enters Execution Phase – The IIJA, which authorized $1.2 trillion in infrastructure spending, is approaching a key deadline as its authorization expires on September 30, 2026. According to the U.S. Department of Transportation, $545.7 billion in adjusted budget authority was available under the IIJA as of April 2026 (latest available), of which $490.2 billion had been announced through grants, $365.7 billion had been obligated and $218.6 billion had been outlaid. These figures represent 67.0% of available funding obligated and 40.1% outlaid, indicating that a substantial portion of funds remains to be deployed as the deadline approaches.

- Data Centers and AI Infrastructure Drive Demand – Data centers and AI infrastructure have emerged as a primary driver of construction activity. Construction Dive notes that data center construction was “the beating heart of the building industry in 2025,” supported by commitments from major technology firms of up to $500.0 billion for U.S. data center development. These large-scale projects have provided a “bright spot” for builders, with multibillion-dollar developments contributing to elevated construction planning activity and expected to remain a leading trend in 2026. The scale of investment continues to expand significantly. Credit ratings agency Moody’s projects approximately $3.0 trillion in global spending through 2030 to support data center expansion and demand for AI capacity. Similarly, Engineering News-Record notes in a November 2025 (latest available) report that data centers “continue to drive a significant amount of market growth,” following a 55.7% increase in 2024 and estimated growth of 33.4% in 2025 and 24.9% in 2026. This demand extends beyond core facilities to include power generation, substations and related infrastructure. As Macrina Wilkins of the Associated General Contractors of America (“AGC”) stated, AI is “driving demand for data centers, construction, substations, electrical infrastructure.”

- Uneven Conditions Across End Markets – As previously discussed, construction activity remains uneven across end markets, with recent data illustrating the divergence in performance. According to the U.S. Census Bureau, manufacturing construction declined 17.0% year-over-year in March 2026 (latest available), while infrastructure-related categories expanded, including sewage and waste disposal, up 8.5%, and power construction, up 5.1%. Other segments showed more modest growth, with commercial construction increasing 0.9% year-over-year and healthcare rising 2.0%. The AIA further characterizes this imbalance, noting that “different sectors may be described as strong, growing, stalled, or declining.” Data centers are identified as the only sector in the strong category, while healthcare and hotels are classified as growing. In contrast, education, retail, warehouses, and amusement and recreation are considered stalled, and both manufacturing and office construction are categorized as declining. Engineering News-Record similarly reports that growth is being driven by sectors such as data centers, power infrastructure and healthcare, as well as highways and bridges, while segments including retail, warehouses, hotels and education remain comparatively weaker.

- Labor Constraints Ease Marginally but Continue to Limit Capacity – Labor conditions in the architecture and engineering industry show modest signs of easing yet continue to constrain firm capacity. According to the ACEC, the share of firms with open positions remains elevated in the first quarter of 2026 (latest available), with 88.0% reporting at least one opening, though this figure declined by four percentage points from the prior quarter, and the median number of open roles decreased from six to five. At the same time, vacancy intensity has not improved meaningfully, as an average of 7.0% of positions remain unfilled, consistent with the previous quarter, and 19.0% of firms report that at least 10.0% of roles are unfilled. These persistent gaps continue to limit growth capacity, even as firms maintain active recruiting efforts. Hiring expectations remain positive, with 65.0% of firms anticipating increased hiring over the next 12 months, although this represents an 11-point decline year-over-year, indicating a more measured outlook. Broader industry data reinforces these conditions. According to the AGC, 63.0% of firms expect to increase headcount in 2026, yet more than four out of five report difficulty filling both hourly craft and salaried positions, reflecting continued hiring challenges across the industry. At the same time, labor availability remains a limiting factor for project execution, particularly for large-scale developments. As Michael Guckes, chief economist at project information firm ConstructConnect, notes, “Once you literally have every contractor within a state and every surrounding state who’s available getting paid top dollar for [data-center project construction], you just can’t move physically any faster.” Additionally, workforce availability has been affected by immigration enforcement, with 66.0% of firms reporting impacts and 24.0% indicating that subcontractors lost workers as a result.

- Policy and Macroeconomic Uncertainty As a Structural Overhang – Policy and macroeconomic uncertainty continue to act as a persistent headwind for the architecture and engineering industry, influencing both short-term expectations and long-term planning. According to the ACEC, in the first quarter of 2026 (latest available), engineering firms report that political instability and broader economic uncertainty remain among their top concerns, cited by 91.0% and 81.0% of respondents, respectively. Although concerns related to tariffs, inflation and recession risk have eased somewhat, they still affect how companies make decisions about new projects and investments. At the same time, entering 2026, construction activity reflects “ongoing uncertainty and imbalance,” with slower growth and uneven performance across sectors. Tariff policy remains a key challenge, as shifting rules make it difficult for companies to predict costs and plan projects that often take years to complete. Changes in federal spending add another layer of uncertainty, as reductions in funding and government employment are expected to affect the broader economy. In addition, Federal Reserve projections show continued variability in key measures such as economic growth, inflation and unemployment, reinforcing an environment in which businesses must plan with limited visibility into future conditions.

- AI Adoption Within Engineering Firms – AI is increasingly being integrated into engineering firm operations, with adoption accelerating as firms move beyond experimentation toward more formalized strategies. According to the ACEC’s first-quarter 2026 (latest available) “Engineering Business Sentiment” survey, 47.0% of firms report having an AI strategy in place, up 18.0 percentage points from 2025, while the share of firms not pursuing AI declined to 22.0%. Leaders also report strong expectations for near-term impact, with 86.0% indicating that AI will positively affect their firm in the coming year. Furthermore, firms are increasingly aligning staffing and investment decisions with this shift, as a majority have either implemented or are planning to hire for AI-focused roles. Beyond strategy and staffing, AI is being deployed to automate routine tasks, accelerate data analysis and improve design efficiency, allowing engineers to focus on higher-value activities such as complex design and decision-making. As adoption expands, executives estimate that an average of 58.0% of their workforce can adapt to new digital skills and processes associated with AI integration.

Recent M&A Trends for the Architecture and Engineering Industry

According to management consulting and research firm Morrissey Goodale, M&A activity in the architecture and engineering industry remained strong through the first half of 2025 (latest available), reflecting continued consolidation across the sector. The firm recorded 250 transactions during the period, consistent with activity levels in both 2024 and 2023, and marking the fifth consecutive year in which annual deal volume was on pace to exceed 450 transactions. This steady level of activity, despite changing economic conditions, suggested a stable and active M&A environment, driven by firms seeking growth, ownership transitions and strategic repositioning, as well as continued access to capital.

A growing share of this activity was driven by repeat acquirers, as 33 firms accounted for 37.0% of all transactions in the first half of 2025, with several completing five or more acquisitions. At the same time, Morrissey Goodale notes that the mix of buyers continues to shift. Employee-owned firms represented 47.0% of transactions, while private equity (“PE”) firms accounted for 45.0%, indicating a narrowing gap between the two groups. Notably, nearly 40.0% of all deals were add-on acquisitions completed by existing PE-backed platforms, highlighting the increasing role of institutional investors in industry consolidation.

From a market standpoint, Morrissey Goodale indicates that transaction activity remained broad but was most concentrated in firms serving buildings and facilities markets, which accounted for 37.0% of total deals in the first half of 2025. Investment also continued to target firms with exposure to transportation, power and water infrastructure. Larger transactions are playing an increasingly important role in overall deal value. Nine transactions in the first half of 2025 involved firms that generated more than $100.0 million in revenue. While these deals represented only 4.0% of total transaction volume, they accounted for a disproportionate share of value, contributing to nearly $5.0 billion in acquired revenue, a 5.0% increase compared with the same period in 2024. This trend reflects a broader shift in the market, as large-scale transactions have become more common in recent years, with 70 such deals completed since 2021, including a record 25 in 2024. As a result, these transactions are playing a more central role in how capital is deployed, platforms are scaled and market leadership is established. In addition, international interest in the U.S. market was strong, with 21 cross-border acquisitions recorded in the first half of 2025, already matching the full-year 2024 total.

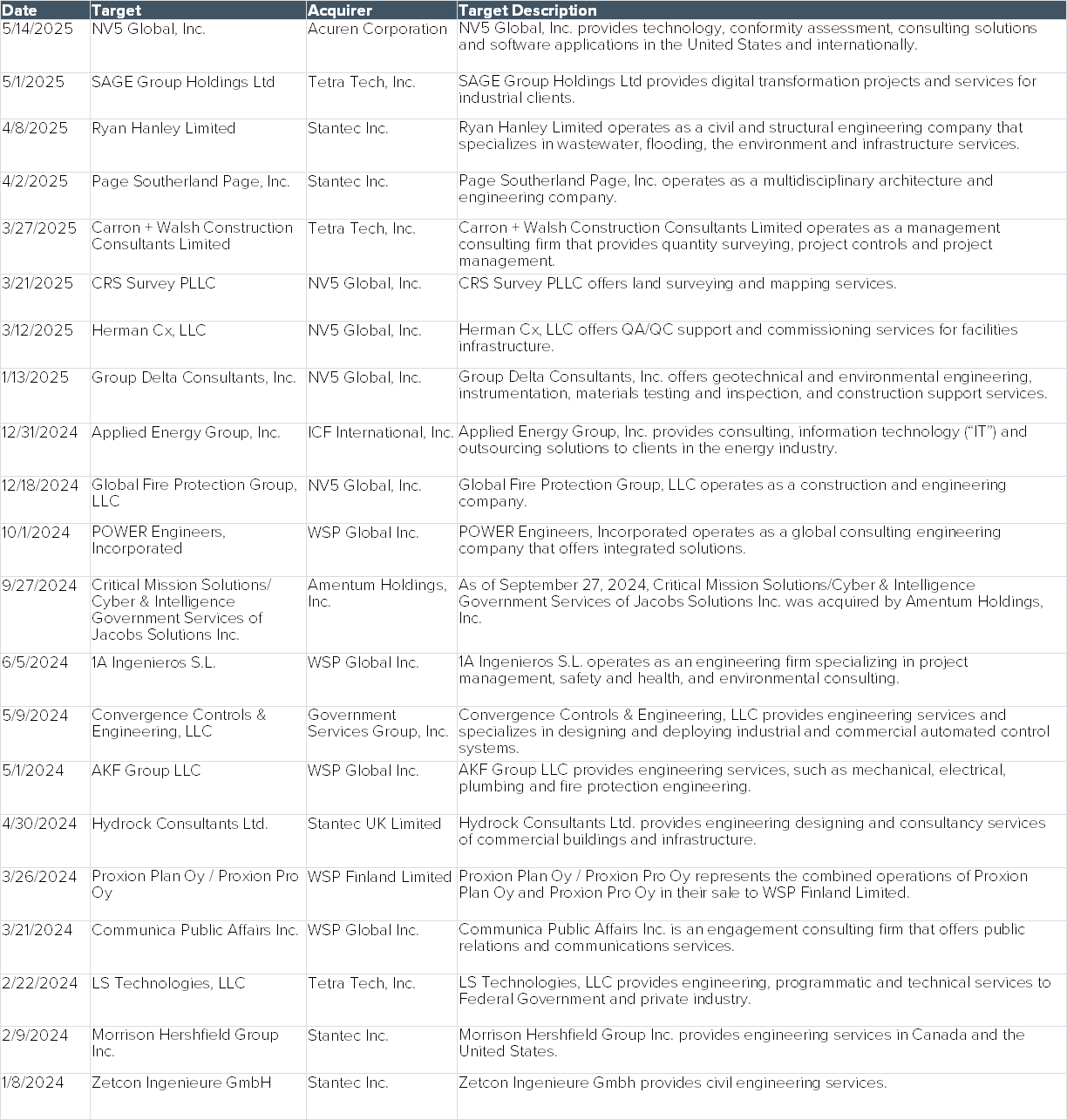

Activity in the M&A market continued through the second half of 2025 and into the early part of 2026, with several transactions involving architecture and engineering firms, including the following:

- In August 2025, Tomball, TX-based Acuren completed its merger with NV5 Global, creating a North American provider of testing, inspection, certification, compliance and engineering services with more than $2.0 billion in revenue. The transaction expanded Acuren’s service offerings and end-market exposure across infrastructure, energy, utilities, government and data center sectors.

- In August 2025, Transcat, Inc. acquired Walsh Engineering Services, Inc. for $84.0 million. The transaction added 113 employees to Transcat’s team and was supported by the company’s recently announced $150.0 million syndicated credit facility jointly led by M&T Bank and Wells Fargo Bank.

- In December 2025, Reston, VA-based Bowman acquired Houston-based RPT Alliance, a designer of natural gas transmission facilities and power generation infrastructure for data centers, industrial facilities and utility operators. The $59.7 million acquisition expanded Bowman’s power and utilities capabilities and strengthened its position in utility-scale power generation and energy infrastructure markets.

- In January 2026, Baar, Switzerland-based SGS completed its acquisition of Applied Technical Services, a North American provider of specialized testing, inspection, calibration and forensics solutions. The acquisition added approximately 2,100 employees and supported SGS’s objective to more than double its North American sales by 2027.

- In March 2026, Reston, VA-based Leidos completed its approximately $2.4 billion acquisition of ENTRUST Solutions Group from private equity firm Kohlberg. The acquisition doubled Leidos’ presence in the energy infrastructure market, expanded its engineering capabilities across the power delivery spectrum, and added more than 3,100 professionals specializing in electric grid engineering and natural gas infrastructure.

Public Company Performance

Recent earnings reports from several large public engineering and consulting firms provide additional perspective on current market conditions and demand trends across the architecture and engineering industry:

- Jacobs Solutions Inc. (“Jacobs”) – For the second quarter of fiscal year (“FY”) 2026, which ended March 27, 2026 (latest available), Jacobs generated $3.7 billion in gross revenue, representing a 27.0% year-over-year increase, with continued expansion in adjusted net revenue and earnings. Adjusted net revenue rose 8.8% to $2.3 billion, and backlog reached $27.0 billion during the quarter, up 21.7%. Bob Pragada, Jacobs’ chair and CEO, stated, “We delivered excellent second quarter results driven by revenue strength in both Infrastructure & Advanced Facilities (I&AF) and PA Consulting. Within I&AF, revenue growth was broad-based, led by the Data Center, Semiconductor, Water, Energy & Power and Transportation sectors. Additionally, PA Consulting grew revenue by 17% year-on-year in Q2, the fourth consecutive quarter of double-digit top line growth.” Consequently, Jacobs raised its full-year fiscal 2026 outlook, with adjusted net revenue expected to grow between 8.0% and 10.5% year-over-year and adjusted earnings before interest, taxes, depreciation and amortization (“EBITDA”) margin projected to range from 14.6% to 14.9%.

- TIC Solutions, Inc. (“TIC Solutions”) – Following its August 2025 combination with NV5, TIC Solutions reported 2025 revenue of $1.5 billion, reflecting a 39.0% increase from the previous year’s combined revenue of approximately $1.1 billion, while adjusted EBITDA rose 25.0% to $234.1 million. Then, during the first quarter of 2026 (latest available), TIC Solutions generated revenue of $488.0 million, up 108.0% year-over-year (primarily reflecting the inclusion of NV5 results), while adjusted EBITDA rose 123.0% to $57.7 million. “We are off to a healthy start in 2026, with first quarter results reflecting the scale and diversity of our combined platform,” said Ben Heraud, CEO of TIC Solutions. “Demand remained resilient across many of our core recurring and compliance-driven service lines, and the business continued to benefit from attractive exposure to transportation infrastructure, manufacturing, midstream energy, data centers, and geospatial analytics.” As a result of strong performance in the first quarter of 2026 and continued integration progress, TIC Solutions reaffirmed its full-year 2026 outlook, with revenue expected to range from $2.15 billion to $2.25 billion.

- Stantec, Inc. (“Stantec”) – Building on continued momentum, Stantec delivered another record-setting year in 2025 (latest available), with net revenue increasing 10.7% year-over-year to $6.5 billion, driven by 5.0% organic growth and 3.9% acquisition growth. Adjusted EBITDA increased 16.7% to $1.1 billion, with margin expanding by 90.0 basis points to 17.6%. In the first quarter of 2026, which ended on March 31, 2026 (latest available), Stantec reported net revenue of $1.7 billion, representing a 9.1% year-over-year increase, driven by 3.6% organic growth and 7.2% acquisition growth. Adjusted EBITDA increased 13.8% to $287.0 million, with margin expanding by 70.0 basis points to 16.9%. “We continue to see strong organic growth in our contract backlog which reached a record $9.0 billion, providing strong visibility into future growth across the markets we serve,” stated Gord Johnston, President and CEO of Stantec. The firm anticipates net revenue growth of 8.5% to 11.5% in 2026

- Tetra Tech, Inc. (“Tetra Tech”) – Tetra Tech reported revenue of $1.21 billion for the first quarter of FY 2026, which ended December 28, 2025, with net revenue of $1.04 billion. Operating income totaled $141.0 million, and adjusted EBITDA was $147.0 million, with adjusted EBITDA margin expanding by 140.0 basis points year-over-year. Backlog stood at $4.0 billion by the end of the quarter. Meanwhile, in its fiscal second quarter of 2026, which ended March 29, 2026 (latest available), Tetra Tech’s revenue was $1.22 billion and net revenue was $1.05 billion. Operating income for the second quarter totaled $132.0 million, and EBITDA was $146.0 million. Further, EBITDA margin increased 90.0 basis points year-over-year, and backlog increased to $4.3 billion, up 8.0% sequentially. Roger Argus, CEO of Tetra Tech, noted, “We delivered a strong second quarter, driven by growth across our end markets in water, environment, and sustainable infrastructure. In U.S. federal, we saw increased orders from defense agencies related to new facilities and infrastructure modernization. Our high-end consulting services for providing water supplies and mitigating environmental impacts are increasingly critical to gaining community support for the establishment of data centers. Our international operations grew due to demand for front-end water and infrastructure consulting services.” For FY 2026, Tetra Tech increased its full-year net revenue projections from $4.25 billion to $4.40 billion.

- WSP Global (“WSP”) – In 2025, WSP reported revenue of $18.3 billion and net revenue of $14.0 billion. Adjusted EBITDA totaled $2.6 billion, reflecting continued operational strength and profitability across the business. Then, during the first quarter of 2026, which ended March 27, 2026 (latest available), WSP generated revenue of $4.6 billion, up 3.7% year-over-year, while net revenue increased 10.8% to $3.7 billion. Adjusted EBITDA rose 16.5% to $622.2 million, and adjusted EBITDA margin expanded 80.0 basis points to 16.8%, driven primarily by improved productivity. In addition, backlog reached a record $19.7 billion, up 19.0%, following the completion of the acquisition of TRC Companies. Alexandre L’Heureux, president and CEO of WSP, stated, “I am pleased with the solid start to the year, with net revenue in line with expectations and strong profitability at the higher end of our adjusted EBITDA outlook range. Our backlog and pipeline remain very active, underscoring the strength of our globally diversified platform.” For full-year 2026, WSP projects net revenue between $16.0 billion and $17.0 billion

- AECOM – For the second quarter of FY 2026, ended March 31, 2026 (latest available), AECOM reported revenue of $3.8 billion and net service revenue of $1.9 billion, representing a 2.0% year-over-year increase on a constant-currency basis. Adjusted EBITDA rose 8.0% to $312.1 million, while adjusted EBITDA margin expanded 20.0 basis points to 16.5%. The company also reported total backlog of $26.2 billion, up 8.0% and marking a record high. “Our strong second quarter and fiscal year-to-date performance highlights the strength and resiliency of our business,” said Troy Rudd, AECOM’s chairman and CEO. “Our competitive advantages of scale, infrastructure domain and technical expertise, and strong client relationships are key to our successes. We are continuing to invest at record levels to enhance our client value proposition and expand our addressable market, which includes our proprietary AI investments and growing our Advisory practice. For full-year FY 2026, AECOM projects adjusted EBITDA between $1.3 billion and $1.3 billion and adjusted diluted earnings per share between $5.90 and $6.10.

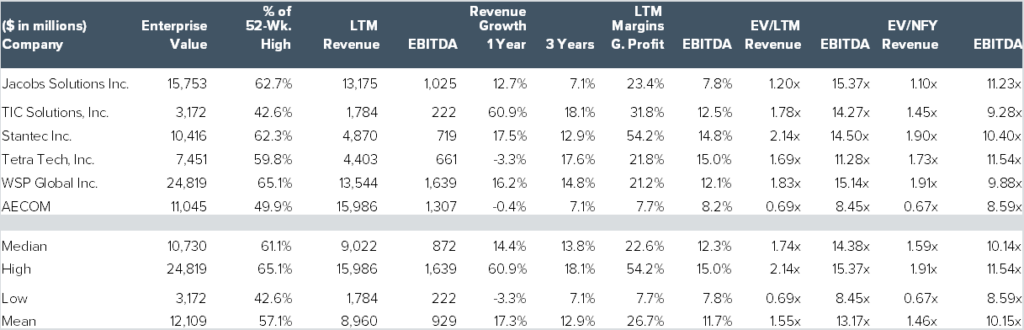

Publicly-Traded Architecture & Engineering Firms

Market information as of: May 15, 2026

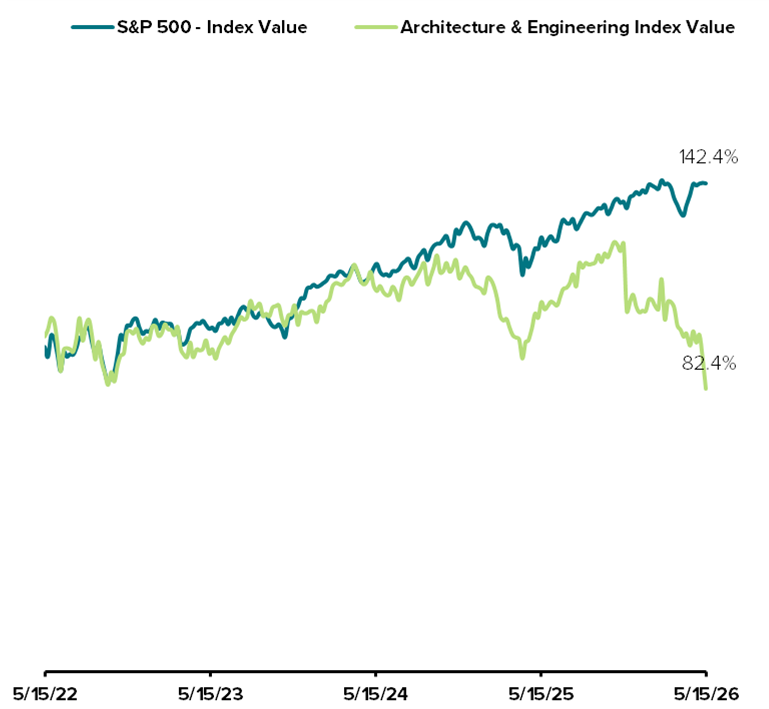

Architecture & Engineering Index Performance vs. S&P 500

Sources: S&P Capital IQ and Public Data

Despite strong operating performance among many large A&E firms, public market valuations in the sector have lagged the broader market. This underperformance reflects investor concerns regarding the industry’s uneven growth profile, as demand has become increasingly concentrated in infrastructure, data center and AI-related projects, while traditional end markets such as office, retail and manufacturing construction continue to face pressure from elevated interest rates and economic uncertainty. In addition, ongoing labor shortages, tariff uncertainty and slowing design contract activity have tempered broader growth expectations, contributing to more cautious investor sentiment despite favorable long-term fundamentals supported by IIJA spending and technology infrastructure investment.

Notable Closed M&A Transactions — Architecture & Engineering Industry

Sources: S&P Capital IQ and Public Data

Henry Ventura is a Director at Prairie Capital Advisors, Inc. and can be contacted at 404.809.2444 or by email, hventura@prairiecap.com.

Download the PDF file above.

Let's Talk

Contact Our Architecture and Engineering Experts