Construction activity in 2025 delivered mixed results, supported by continued strength in select segments even as broader economic and policy uncertainty weighed on the industry. Looking ahead, contractors remain cautiously optimistic, though expectations for 2026 are tempered by concerns surrounding interest rates, federal policy, labor availability and rising material costs driven in part by tariffs. Forecasts suggest mixed performance across construction segments in 2026, while also pointing to the growing risk that persistent instability could slow decision making and investment across the market.

Recent Industry Performance

According to Dodge Construction Network (“Dodge”), during 2025, total construction starts increased 5.4% to reach $1.24 trillion. Broken down further, nonresidential starts rose 4.5% and nonbuilding starts were up 18.7% when compared to 2024, while residential starts declined 4.8%.

Moving forward, Dodge expects construction activity to remain supported by select large-scale projects, even as uncertainty continues to weigh on the broader market. Sarah Martin, associate director of forecasting at Dodge, notes, “Megaprojects, led by data centers, will keep construction activity afloat next year, but persistent downside risks will limit the overall outlook.”

In a September 2025 (latest available) outlook, Dodge forecasts that the total dollar value of U.S. construction starts will decline by 0.4% in 2026. Nonresidential starts are projected to increase by 1.3% and residential starts are expected to rise by 1.7%, while nonbuilding starts will likely drop by 4.4%.

Moreover, Martin points to continued ambiguity surrounding tariffs and other federal policies as the primary risk facing the construction market, describing policy-driven volatility as “the biggest threat” to the economic outlook and noting that both consumers and businesses may delay investment decisions in response. While those pauses are manageable in the short term, Martin cautions that they are ultimately constrained by underlying financial strength: “While, in aggregate, both consumers and businesses remain in decent financial shape, there is a distribution in financial strength that will be increasingly revealed and tested should policy uncertainty linger.”

Nonresidential Construction

As previously mentioned, Dodge reports that in 2025, U.S. nonresidential construction starts grew 4.5% when compared to 2024, reaching $473.0 billion. Within the segment, commercial and industrial starts increased by 10.9%, while institutional starts declined by 1.9% in 2025 compared with the previous year.

At the same time, project information firm ConstructConnect offers a different perspective on nonresidential building starts in 2025. The firm reports that nonresidential building starts totaled $482.1 billion in 2025, rising 18.6% from 2024. Broken down further, commercial starts increased by 22.4% and manufacturing starts expanded by 84.2%, while institutional starts fell by 5.4%. Moreover, ConstructConnect notes the following pattern for the commercial sector in 2025: hotel/motel, down 24.9%; retail/shopping, up 1.1%; retail miscellaneous, up 0.4%; parking garages, down 12.3%; amusement, down 11.0%; private office, up 110.9%; government office, down 2.1%; laboratory, down 9.7%; warehouse, down 14.4%; sports stadium/convention centers, up 9.3%; and transportation terminals, down 13.4%. Within the institutional category, specific segments saw the following pattern in 2025: religious, up 22.9%; hospital/clinic, down 18.9%; nursing/assisted living, up 39.2%; library/museum, down 0.4%; courthouses, down 10.1%; police stations and fire halls, up 14.9%; prisons, down 34.6%; military, up 24.5%; pre-school/elementary, up 0.2%; junior and senior high schools, down 1.1%; special and vocational schools, down 32.7%; colleges and universities, down 5.2%; and miscellaneous medical, down 18.1%.

Looking ahead, Dodge’s September 2025 (latest available) forecast indicates that total nonresidential construction starts are expected to increase 3.0% in 2026, supported by ongoing data center development and the initiation of several large-scale megaprojects. Specifically, commercial construction starts are projected to rise 7.0% in 2026, with growth becoming more balanced across segments as activity in retail, warehouse and hotel construction begins to recover. Dodge also notes that additional Federal Reserve rate cuts and firmer business and consumer spending are expected to contribute to that acceleration. Institutional construction starts are expected to grow modestly, as increased activity in healthcare and recreational facilities is offset by slower growth in the education, dormitory and transportation segments. Moreover, Dodge expects manufacturing construction activity to moderate as the elevated cost-per-square-foot dynamics associated with recent semiconductor projects begin to normalize. Manufacturing construction dollar value is projected to decline 24.0% during 2026, while square footage is expected to fall by a more moderate 7.0%. This reflects a pullback from earlier high-value projects, even as underlying activity remains constrained. The forecast assumes that potential onshoring or reshoring of manufacturing capacity will provide only limited support to construction activity over the medium term.

Meanwhile, ConstructConnect projects that total nonresidential building starts will decline by 6.7% in 2026, with manufacturing starts contracting 20.4%, commercial starts falling 3.2% and institutional starts down 2.2%. Specifically, the manufacturing segment is expected to decline as pipeline maturity and a slowdown in megaproject starts weigh on activity. Within the commercial segment, all categories are expected to decline except shopping retail, with the steepest contractions projected in government offices, laboratories (schools and industrial) and transportation terminals. At the same time, within the institutional segment, ConstructConnect forecasts gains in hospitals/clinics and military construction, partially offset by expected declines in educational facilities.

Looking longer term, ConstructConnect projects that total nonresidential building starts will grow by 3.6% in 2027, 4.2% in 2028 and 3.7% in 2029.

Residential Construction

Dodge reports that residential construction starts contracted 4.8% in 2025, reaching $374.0 billion. Specifically, single-family starts were down 13.2% year-over-year, while multifamily starts were up 13.1%.

Meanwhile, the National Association of Home Builders (“NAHB”) notes that, in October 2025 (latest available), total housing starts reached a seasonally adjusted annual rate (“SAAR”) of 1.25 million, down from 1.31 million in September 2025. Due to the government shutdown from October 1 to November 12, 2025, data beyond October 2025 was not available as of this writing. For comparison, total housing starts in October 2024 registered a SAAR of 1.35 million. Broken down further, single-family starts registered a SAAR of 874,000 in October 2025, a decrease from the 948,000 in October 2024, while multifamily housing starts reached a SAAR of 372,000, a decline from the 404,000 in October 2024. Moreover, the NAHB reports that, on a regional basis, total housing starts rose in the Northeast at a SAAR of 154,000 while falling in the Midwest, South, and West, at SAARs of 199,000; 650,000; and 243,000, respectively.

Moving forward, the NAHB projects that single-family construction will increase by 7.5% in 2026, and multifamily construction will rebound by an estimated 10.5%. “Builders continue to grapple with market and macroeconomic uncertainty,” notes Danushka Nanayakkara-Skillington, assistant vice president of forecasting and analysis at the NAHB, adding, “Single-family starts will grow slowly in the years ahead.”

Dodge is less optimistic than the NAHB in a September 2025 (latest available) outlook. The firm forecasts that residential construction starts will increase by 1.7% in 2026, with single-family starts down 1.9% and multifamily starts up 7.6%. Dodge notes, “While mortgage rates have ticked down recently, the elevated risk of recession and ongoing economic uncertainty is keeping homebuyers on the sidelines.”

At the same time, ConstructConnect forecasts 9.9% growth in the residential construction market in 2026, followed by increases of 5.9% in 2027, 6.7% in 2028, and 7.7% in 2029. In 2026, single-family and multifamily starts are expected to rise by 11.4% and 6.8%, respectively.

Additionally, the Leading Indicator of Remodeling Activity, published by the Remodeling Futures Program (“RFP”) at the Joint Center for Housing Studies of Harvard University (“Joint Center”) notes that annual spending on improvements and maintenance is expected to gradually slow through 2026. Year-over-year, spending on home improvements and repairs is forecast to increase 2.9% in early 2026, then ease to 1.6% by the end of the year. “Single-family home sales and permitting activity have picked up modestly from very low levels, which should support a nominal increase in remodeling activity this year,” says Rachel Bogardus Drew, director of the RFP at the Joint Center. “Even with some deceleration later in the year, overall annual homeowner spending on improvements is expected to reach $552.0 billion by the end of 2026.”

According to Chris Herbert, managing director of the Joint Center, “Remodeling trends closely track the health of the broader housing market.” Herbert went on to say, “If interest rates begin to ease, that could provide a much-needed boost to both housing construction and retail sales of building materials, which for now continue to pose significant headwinds to homeowner improvement spending.”

Nonbuilding Construction

According to Dodge, nonbuilding construction starts grew by 18.7% in 2025, reaching a total of $396.0 billion. Meanwhile, ConstructConnect notes that heavy/civil engineering starts totaled $314.6 billion in 2025, up 13.9% from 2024, with specific segments seeing the following pattern: airport, up 47.4%; road/highway, up 8.9%; bridge, up 4.9%; dam/marine, up 10.2%; water/sewage, up 6.8%; electric power infrastructure, up 37.6%; and all other civil, up 16.1%.

Notably, in March 2025, the American Society of Civil Engineers (“ASCE”) released its “2025 Report Card for America’s Infrastructure” (“Report Card”), assigning U.S. infrastructure an overall grade of C. This marks the highest grade since the ASCE began issuing report cards in 1998 and is an improvement from the C- awarded in 2021. Specifically, eight infrastructure categories improved, seven were unchanged and two declined. The ASCE attributed the overall progress to increased infrastructure investment since the prior report, including funding from the Infrastructure Investment and Jobs Act of 2021 (“IIJA”) and the Inflation Reduction Act of 2022 (“IRA”). Despite recent funding gains, the ASCE cautions that an overall grade of C still reflects widespread deterioration across U.S. infrastructure and the need for continued investment. Further, consulting firm McKinsey & Co. estimates that several sectors remain significantly underfunded, including the U.S. water utility sector, which faced an estimated $110.0 billion funding gap in 2024. This gap encompassed nearly 60.0% of total sector spending and is projected to widen to approximately $194.0 billion by 2030.

Infrastructure funding faced additional uncertainty in 2025 after President Trump froze payments from the IIJA and IRA on his first day in office, according to Construction Dive. In March 2025, six nonprofits sued several federal agencies seeking access to previously awarded funds after earlier court efforts failed. In mid-April 2025, a federal judge in Rhode Island ordered the release of the frozen funds, finding the agencies lacked authority to halt disbursements. The ruling remains a preliminary injunction, allowing funding to flow while litigation continues.

Additionally, Construction Dive reports that in July 2025, the Trump administration outlined infrastructure priorities focused on permitting reform and faster project delivery. Transportation Secretary Sean Duffy emphasized streamlining regulations and signed an agreement allowing the Texas Department of Transportation (“DOT”) to assume greater environmental permitting authority, while encouraging other states to take on National Environmental Policy Act responsibilities. Moreover, the DOT announced $488.0 million in Better Utilizing Investments to Leverage Development grants for 30 projects nationwide and said it would reallocate $4.0 billion in unspent funding from California’s high-speed rail project.

Looking ahead, in its September 2025 (latest available) forecast, Dodge projects that total nonbuilding construction starts will fall 4.4% in 2026, with specific segments projected as follows: environmental public works, up 5.2%; other nonbuilding, down 8.7%; power plants/gas/communications, down 20.0%; and highways and bridges, up 2.9%.

Meanwhile, the American Road and Transportation Builders Association (“ARTBA”) projects that highway construction will increase 2.3% in 2026. “Growth is expected to moderate as we enter the last year of the current federal-aid highway law,” notes Alison Premo Black, senior vice president and chief economist at ARTBA. “Federal and state investments continue to support ongoing construction activity, with a focus on bridge work and major improvements.”

At the same time, ConstructConnect anticipates that heavy/civil engineering starts will increase 3.4% in 2026, followed by growth of 4.3% in 2027, 3.8% in 2028 and 2.8% in 2029. Growth in 2025 is attributed to increased activity in airport construction (up an estimated 14.2%), road construction (up 7.7%) and bridge construction (up 7.6%), supported in part by infrastructure grant programs. Notably, miscellaneous civil is the only subsector projected to decrease, falling an estimated 11.6%. Indeed, ongoing investment in transport networks, resilient water infrastructure and bridge replacement is expected to support sector stability despite continued constraints in other civil areas.

Construction Industry Trends/Drivers

Construction Input Prices

According to the U.S. Bureau of Labor Statistics (“BLS”), construction input prices were up 0.6% in November 2025 (latest available, due to the aforementioned government shutdown) when compared to October 2025, and overall costs were 3.4% higher than the same period in 2024. This increase is attributed to tariffs imposed by the Trump administration. “Construction input prices surged in November and are now up 3.4% on a year-over-year basis,” notes Anirban Basu, chief economist of Associated Builders and Contractors (“ABC”). “While that’s a relatively modest annual increase, it’s also the largest since January 2023 and the trend offers plenty of cause for concern. Many tariff-affected materials, like derivative metal products and switchgear equipment, have experienced considerable price escalation in 2025. Prices for aluminum mill shapes and primary and secondary nonferrous metals are both up more than 25% over the past year.” At the same time, Associated General Contractors of America (“AGC”) Chief Economist Ken Simonson indicates, “Input costs for construction are rising faster than for producers or consumers in general, partly because the industry is faced with steep tariffs on many materials.” Simonson went on to add, “Although many contractors are accelerating purchases and attempting to pass along cost increases, their bid prices have not kept up, rising only 2.7% in the past 12 months.”

Labor Issues

The BLS reports that construction industry employment increased by 14,000 jobs, or 0.2%, in 2025. However, ABC’s Basu notes, “Excluding the first year of the COVID-19 pandemic, that’s the worst 12-month performance since 2011, when the construction industry was still spiraling from the Great Recession.” Still, construction unemployment remains low, down 0.2 percentage points year-over-year. Further, average hourly earnings rose 4.5% year-over-year in November and December 2025, but falling backlogs, lower spending and job losses suggest a challenging start to 2026 despite hiring optimism. Meanwhile, a recent AGC survey indicates that labor challenges persist across the industry. Indeed, 82.0% of respondents reported difficulty filling hourly craft positions, while 80.0% experienced difficulty in filling salaried roles, the highest levels since 2023. Furthermore, workforce-related issues were cited, such as an insufficient supply of workers or subcontractors (57.0% of respondents), rising direct labor costs (56.0%) and worker quality (53.0%). Despite these challenges, 63.0% of firms expect to add headcount in 2026. To address labor and productivity pressures, construction firms are increasingly turning to technology, with 61.0% reporting current or planned investment in artificial intelligence (“AI”).

Construction Backlog

ABC notes that its “Construction Backlog Indicator,” which tracks commercial, institutional, heavy industrial and infrastructure construction, rose to 8.2 months in December 2025, up 0.1 month from the previous month and down 0.1 month from December 2024. Backlog trends continue to vary significantly by firm size: contractors generating more than $100.0 million annually reported their strongest backlog since 2021, while firms with under $30.0 million in revenue experienced their weakest backlog levels over the same period.

Construction Confidence Index

The three metrics measured by ABC’s “Construction Confidence Index” (sales, profit margins and staffing) remained above 50.0 in December 2025, indicating expected growth in 2026. All three increased month-over-month but remained below December 2024 levels. “Backlog fell sharply for smaller contractors during 2025,” notes ABC’s Basu. “That decline was largely due to the fact that nonresidential construction momentum is confined to the data center segment, and those projects are far more beneficial for the largest contractors. In December, the 13% of ABC members under contract to work on a data center project had significantly higher backlog (11.0 months) than those who were not (7.8 months). While contractor confidence improved slightly for the month, it remains well below late-2024 and early-2025 levels.”

NAHB Builder Confidence Survey

According to the NAHB/Wells Fargo Housing Market Index (“HMI”), builder confidence fell in January 2025 as affordability concerns continue to weigh heavily with buyers, and builders continue to contend with rising construction costs. Indeed, the HMI rose two points to 37.0 in January 2025. (The HMI measures builder perceptions for the following six months on a scale of “good,” “fair” or “poor.” Any reading above 50.0 indicates that builders view the outlook as positive.) All HMI subindices declined in January 2025. The measure of current sales conditions slipped one point to 41.0, while the index tracking prospective buyer traffic fell to 23.0, dropping three points. The future sales index also dropped three points to 49.0, marking its first move below the 50.0 breakeven level since September 2025. “While the upper end of the housing market is holding steady, affordability conditions are taking a toll on the lower and mid-range sectors,” said NAHB Chairman Buddy Hughes. “Buyers are concerned about high home prices and mortgage rates, with downpayments particularly challenging given elevated price to income ratios.”

Immigration Enforcement

Construction Dive indicates that approximately a year into President Trump’s second term, contractors are not yet experiencing widespread immigration enforcement on construction jobsites. Ken Simonson, chief economist at the AGC, notes that immigrants account for approximately 34.0% of construction trades workers, with some trades reaching as high as 61.0%, and stated that “the construction inflow of potential workers has been turned off.” At the same time, Brian Turmail, vice president of public affairs and workforce at the AGC, explained that enforcement activity has shifted away from jobsites toward a broader community-wide focus. Contractor groups report that undocumented employees may fail to report to work after being apprehended by Immigration and Customs Enforcement (“ICE”) officers or out of fear of enforcement actions. Separately, attorney Trent Cotney notes “ICE raids and I-9 audits have severely impacted crews,” adding that among his clients, labor pay rates are rising between 4.0% and 10.0% as the workforce contracts in early 2026.

AI Adoption

AI is gaining traction in the construction industry, though adoption remains uneven and varies by firm size. Surveys from the Royal Institution of Chartered Surveyors (“RICS”), BuiltWorlds and a collaboration between Dodge and CMiC indicate that while most contractors recognize AI’s potential, nearly half report no current implementation, with another 34.0% limited to pilot programs. Additionally, larger firms are adopting AI more rapidly, with companies generating more than $5.0 billion in revenue significantly more likely to report above-average AI maturity and to view AI as a competitive advantage. Smaller and mid-sized firms, by contrast, more frequently cite cost, data quality and internal expertise as barriers. Despite these challenges, growing investment, pilot activity and staffing efforts suggest the industry is nearing an AI adoption “tipping point.”

Prairie’s 2025 Construction Survey

Prairie’s 6th Annual ESOP Construction Survey, conducted in November 2025, highlights an industry that remains resilient despite persistent macroeconomic challenges. Survey respondents from construction companies with employee stock ownership plans reported stable backlogs and solid demand entering 2026, with several firms achieving record performance driven by data center and infrastructure-related work. While elevated interest rates, labor constraints and competitive bidding continue to pressure operations, firms expressed cautious optimism for 2026, particularly if interest rates decline further. Respondents also pointed to employee ownership as a key differentiator, supporting strong culture, accountability and retention during a period of ongoing uncertainty. For more information, see Prairie’s 6th Annual ESOP Construction Survey.

Read Prairie’s 6th Annual Construction Survey

Recent M&A Trends for the Construction Industry

According to PwC, global mergers and acquisitions (“M&A”) momentum heading into 2026 suggests the market is entering a new phase rather than simply rebounding from a subdued cycle. A surge in megadeals late in 2025 drove a sharp increase in overall deal value, even as deal volumes remain relatively flat, resulting in what PwC characterizes as an increasingly K-shaped M&A market. In 2025, global deal values rose by 36.0%, fueled by approximately 600 transactions valued above $1.0 billion, while value across the remaining roughly 47,000 transactions was flat year-over-year. PwC notes that confidence has returned at the top end of the market, supported by well-capitalized buyers and large strategic transactions, while mid-market and smaller deals remain constrained by valuation gaps and execution risk, as well as lingering macroeconomic and geopolitical uncertainty. As Brian Levy, PwC’s global deals industries leader, observes, “Confidence has clearly returned at the top end, while activity elsewhere remains more constrained.”

With regard to the domestic construction and engineering sector, PwC reports that dealmaking regained momentum in the second half of 2025 after a cautious first half, though overall activity remained below 2024 levels. Furthermore, M&A in the sector has increasingly been driven by efforts to address rising material costs, persistent labor shortages and policy-related shifts, with buyers using acquisitions to strengthen domestic capacity, improve supply chain resilience and pursue productivity gains.

Following are several notable transactions that took place in the construction and engineering industry in the second half of 2025:

- TopBuild Corp, Inc. (“TopBuild”) Acquires Progressive Roofing – On July 15, 2025, insulation and commercial roofing installer TopBuild announced the acquisition of commercial roofing installation services provider Progressive Roofing in an all-cash transaction valued at $810.0 million. Robert Buck, president and CEO of TopBuild, said, “We want to extend a warm welcome to the Progressive Roofing team. We are excited to establish a new platform for organic and M&A growth in the large and highly complementary commercial roofing services sector. The acquisition not only enables us to provide commercial customers with a comprehensive suite of building envelope solutions but also increases our revenue exposure to non-discretionary revenue demand drivers. Progressive Roofing represents a great opportunity for us to further drive growth and profitability, in turn delivering increased shareholder returns.”

- Quanta Services, Inc. (“Quanta”) Acquires Dynamic Systems, LLC (“Dynamic Systems”) – On July 25, 2025, Quanta Services, a North American specialized contracting company, announced its acquisition of Texas-based mechanical, plumbing and process infrastructure solutions provider Dynamic Systems for approximately $1.35 billion at close, with the potential for an additional $216.0 million tied to post-acquisition financial performance targets. Duke Austin, Quanta’s president and CEO, commented, “We are excited to announce the acquisition of Dynamic Systems and we welcome their employees to the Quanta family…They bring an exceptional management team and a premier craft-skilled workforce that complement Quanta’s culture. Dynamic Systems will enhance Quanta’s comprehensive infrastructure solutions offering that can facilitate innovative speed-to-market solutions for the load center market.”

- CRH Acquires Eco Materials Technologies – On September 22, 2025, CRH, a global provider of building materials, announced the completion of its acquisition of Eco Materials Technologies, a North American producer and supplier of sustainable, near-zero-carbon cement alternatives, for a total consideration of $2.1 billion. According to CRH, the completed acquisition strengthens the company’s position in next-generation cement and concrete products as demand for cementitious materials increases alongside infrastructure investment in North America. The transaction aligns with CRH’s capital allocation strategy and is expected to support future growth.

- Dycom Industries, Inc. (“Dycom”) Acquires Power Solutions, LLC (“Power Solutions”) – On December 23, 2025, U.S. specialty contracting services firm Dycom announced its acquisition of Power Solutions, one of the Mid-Atlantic’s largest electrical contractors, for $1.63 billion. “Today’s announcement represents a significant milestone for Dycom, reinforcing the Company’s position as a leader in the fast-growing digital infrastructure industry,” notes Dan Peyovich, president and CEO of Dycom. “We are excited to officially welcome Power Solutions to the Dycom family and look forward to working together to realize the opportunities ahead.”

Looking ahead, PwC projects that M&A activity in the U.S. construction and engineering sector will be shaped by demand for infrastructure investment, data center development, grid modernization and advanced manufacturing, alongside continued adoption of technology-enabled, labor-efficient solutions. PwC notes that residential construction has remained resilient but disciplined amid high interest rates and tight credit conditions, while deal activity is increasingly focused on targeted, strategic transactions rather than broad-based expansion. PwC adds that as these dynamics extend into 2026, the U.S. construction and engineering sector’s near-term M&A outlook will hinge on how effectively companies scale operations, manage labor and cost pressures, and deploy technologies that enable more efficient and resilient delivery.

Data & Resources

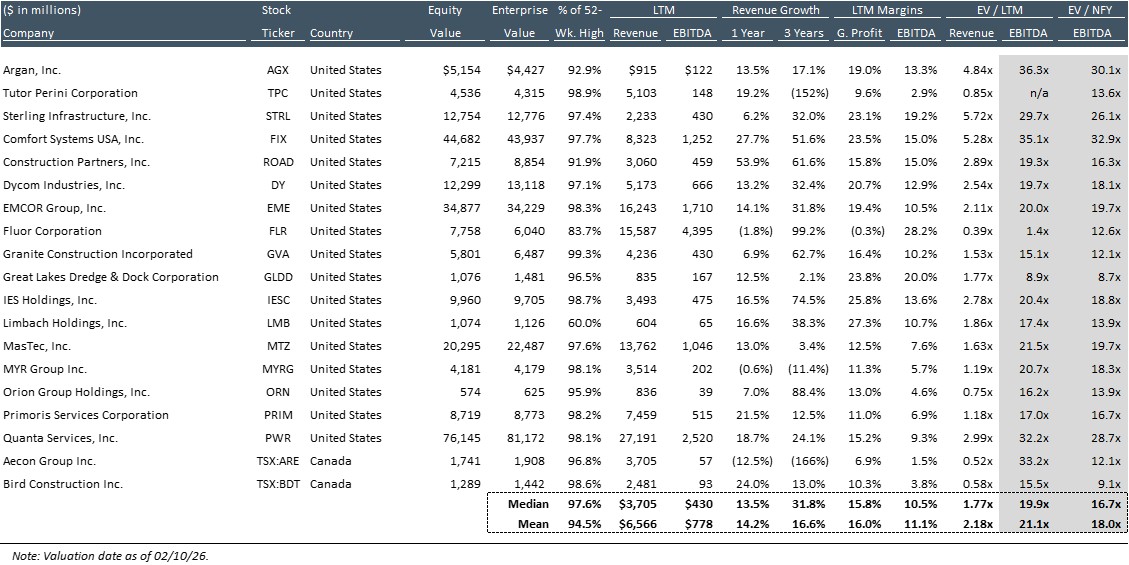

Publicly-Traded Construction Companies

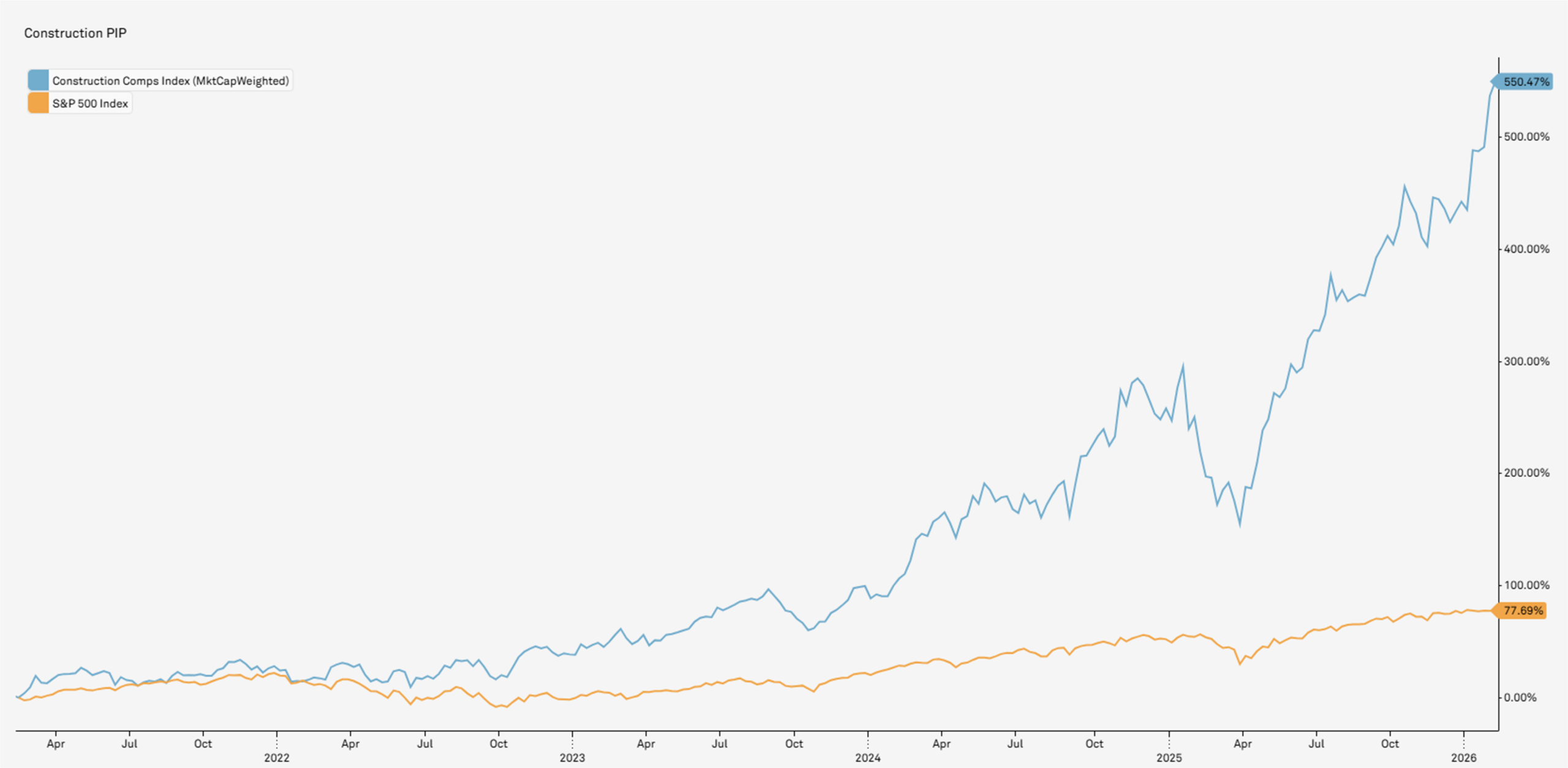

Construction Index Performance vs. S&P 500

Sources: S&P Capital IQ and public data

Construction equities have significantly outpaced the broader market, driven by infrastructure investment, growing data center and industrial project activity, and historically strong backlogs. Improved execution and pricing have supported margin expansion and earnings momentum.

Construction Industry Trends

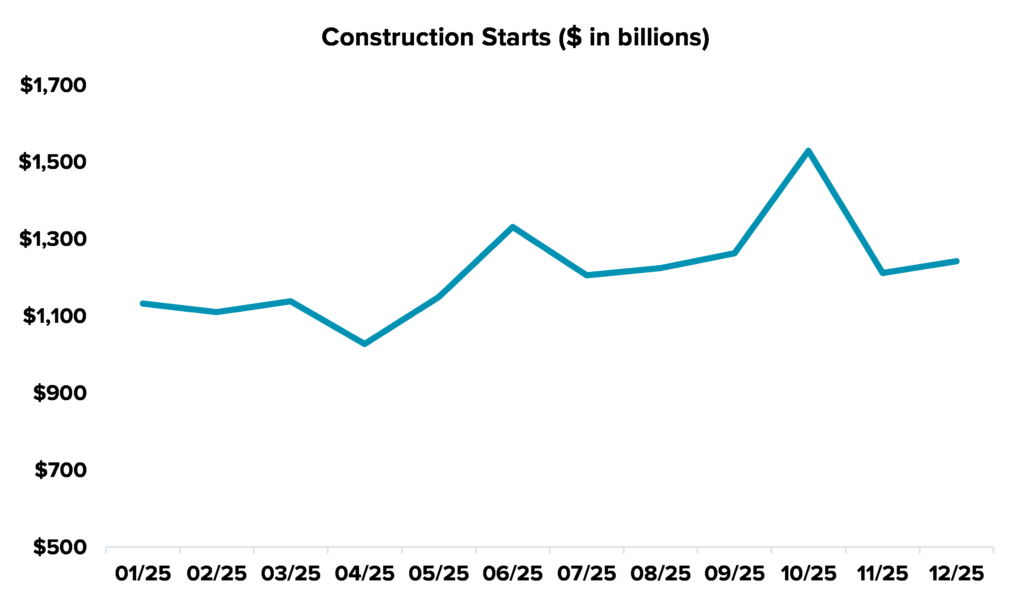

Construction Starts

Source: Dodge Data & Analytics

Dodge Data & Analytics measures the seasonally-adjusted value of total U.S. construction starts each month, as well as the value of starts in nonresiden-tial, residential and nonbuilding categories.

U.S. Construction Jobs

Source: Bureau of Labor Statistics

The Bureau of Labor Statistics releases job gains or losses in the industry and divides the figures into residential and nonresidential sectors.

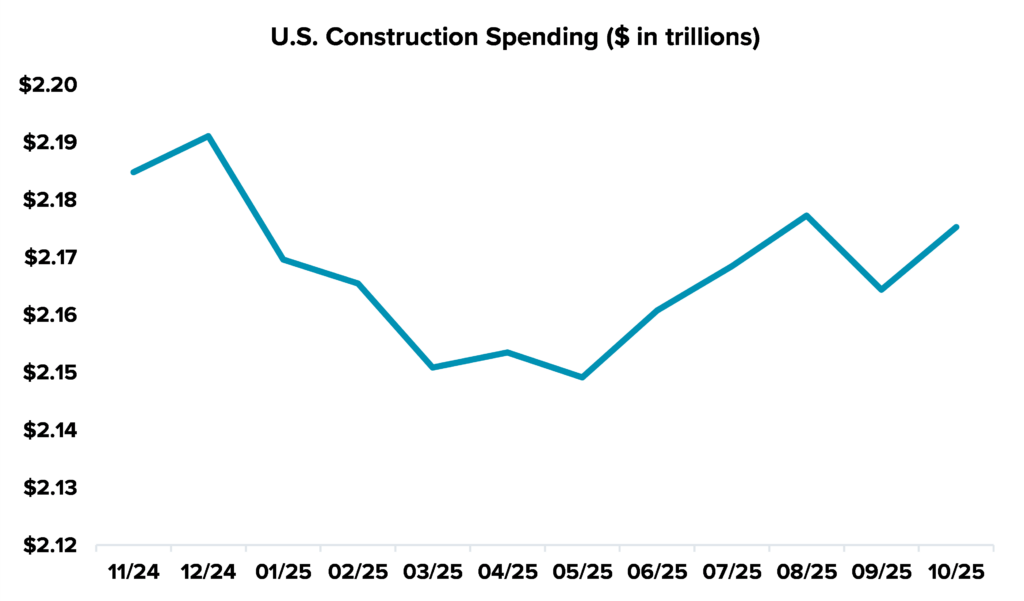

U.S. Construction Spending

Source: U.S. Census Bureau

While often revised in subsequent months, construction spending figures each month from the U.S. Commerce Department examine the private and public construction sectors. Within the private sector, the report tracks single-family residential, multifamily residential and nonresidential starts.

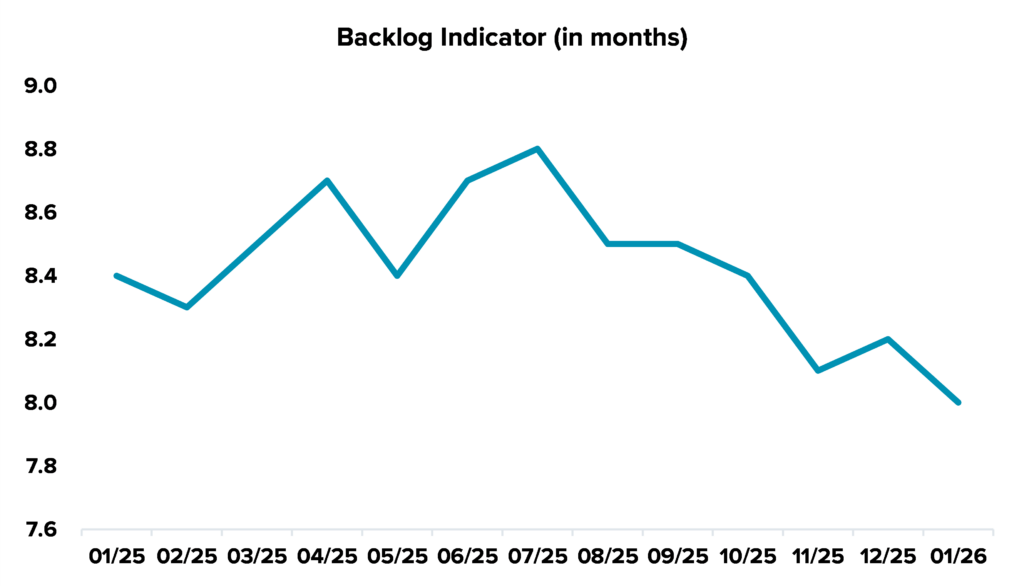

Backlog Indicator

Source: Associated Builders and Contractors

The Associated Builders and Contractors’ backlog indicator is a forwardlooking economic metric that reflects the amount of work under contract that will be performed by commercial and industrial construction contractors in the months ahead.

Notable Closed M&A Transactions — Construction Industry

| # | Date Closed | Target | Acquirer | Classification |

|---|---|---|---|---|

| 1 | 2/10/2026 | Service Painting Corporation | Valcourt Building Services | Subcontractors & Specialty Trade |

| 2 | 2/5/2026 | Jersey Fire Protection Corp | Pye-Barker Fire & Safety | Subcontractors & Specialty Trade |

| 3 | 2/5/2026 | Tucker Hill Air, Plumbing & Electrical | Chill Brothers, LLC | Subcontractors & Specialty Trade |

| 4 | 2/4/2026 | Division 7 Building Contractors, Inc. | Royalty Companies of Indiana, Inc. | General Contractors & Heavy Civil Construction |

| 5 | 2/4/2026 | Conco, LLC | Crain Capital, LLC | Civil Engineering & Consulting |

| 6 | 2/4/2026 | Ramos Consulting Services, Inc. | Colliers Engineering & Design, Inc. | Civil Engineering & Consulting |

| 7 | 2/3/2026 | Prism Engineering & Design Group, LLC | Pape-Dawson Engineers, Inc. | Architecture & Engineering (A&E) |

| 8 | 2/3/2026 | Applied Coatings LLC | TopBuild Corp. (NYSE:BLD) | Manufacturing & Building Materials |

| 9 | 2/3/2026 | J.E. Mcamis, Inc. | Orion Group Holdings, Inc. (NYSE:ORN) | General Contractors & Heavy Civil Construction |

| 10 | 2/3/2026 | Cal Engineering Solutions, Inc. | Davey Resource Group, Inc. | Civil Engineering & Consulting |

| 11 | 2/2/2026 | Thermo Tech Mechanical Insulation, Inc. | Installed Building Products, Inc. (NYSE:IBP) | Manufacturing & Building Materials |

| 12 | 2/2/2026 | GMJ Paving Company LLC | Construction Partners, Inc. (NASDAQ:ROAD) | General Contractors & Heavy Civil Construction |

| 13 | 2/2/2026 | Hoffman Planning, Design & Construction, Inc. | Keller, Inc. | General Contractors & Heavy Civil Construction |

| 14 | 2/2/2026 | FSI Engineering and Design, Inc. | Sedgman Limited | Architecture & Engineering (A&E) |

| 15 | 2/2/2026 | Cobalt Power Systems, Inc. | SunPower Inc. (NASDAQ:SPWR) | Renewable Energy & Infrastructure |

| 16 | 1/29/2026 | TechPro Power Group, Inc. | Integrated Power Services, LLC | Industrial & Specialty Services |

| 17 | 1/29/2026 | WGI, Inc. | First Reserve Management, L.P. | Civil Engineering & Consulting |

| 18 | 1/23/2026 | American Roadway Logistics, Inc. | Frontline Road Safety Group, LLC | Industrial & Specialty Services |

| 19 | 1/22/2026 | DLB Associates Consulting Engineers, P.C. | Accenture plc (NYSE:ACN) | Architecture & Engineering (A&E) |

| 20 | 1/22/2026 | Bold North Roofing & Contracting | Ridgeline Roofing & Restoration, LLC | Subcontractors & Specialty Trade |

| 21 | 1/20/2026 | Alacrity Network Solutions, LLC | BV Investment Partners | Industrial & Specialty Trade |

| 22 | 1/20/2026 | Southern Fire Control, LLC | Sciens Building Solutions, LLC | Subcontractors & Specialty Trade |

| 23 | 1/8/2026 | Ivocon, Inc. | Cemtrex, Inc. (NASDAQ:CETX) | Industrial & Specialty Services |

| 24 | 1/5/2026 | Mid Atlantic Storage Systems, LLC | DXP Enterprises, Inc. (NASDAQ:DXPE) | Industrial & Specialty Services |

| 25 | 1/5/2026 | Buford Goff & Associates, Inc. | IMEG Corp. | Architecture & Engineering (A&E) |

| 26 | 1/5/2026 | CFR Engineering Consultants, Inc. | IMEG Corp. | Architecture & Engineering (A&E) |

| 27 | 1/5/2026 | Surface Preparation Technologies, LLC | Frontline Road Safety Group, LLC | Industrial & Specialty Services |

| 28 | 1/2/2026 | The Bowers Group, Inc. | Legence Corp. (NASDAQ:LGN) | Industrial & Specialty Services |

| 29 | 12/23/2025 | Power Solutions, LLC | Dycom Industries, Inc. (NYSE:DY) | Industrial & Specialty Services |

| 30 | 12/20/2025 | NV2A Group, LLC | MasTec, Inc. (NYSE:MTZ) | Industrial & Specialty Services |

| 31 | 12/19/2025 | Pike Corporation | CDPQ; TPG Capital; TPG Rise Climate | General Contractors & Heavy Civil Construction |

| 32 | 12/16/2025 | Service Logic, LLC | Bain Capital, LP; Mubadala Investment Company | Industrial & Specialty Services |

| 33 | 12/5/2025 | United Flow Technologies | Berkshire Partners LLC; H.I.G. Capital, LLC | Industrial & Specialty Services |

| 34 | 12/5/2025 | Rpt Alliance LLC | Bowman Consulting Group Ltd. (NASDAQ:BWMN) | Civil Engineering & Consulting |

| 35 | 11/24/2025 | Ambia Energy, LLC | SunPower Inc. (NASDAQ: SPWR) | Renewable Energy & infrastructure |

| 36 | 11/4/2025 | Pearce Services, LLC | CBRE Group, Inc. (NYSE:CBRE) | Industrial & Specialty Services |

| 37 | 10/1/2025 | RCI Liquidations, Inc. | Cardinal Infrastructure Group, Inc. (NASDAQ:CDNL) | Renewable Energy & Infrastructure |

| 38 | 9/24/2025 | Sunder Energy LLC | Complete Solar, Inc. | Renewable Energy & Infrastructure |

| 39 | 9/2/2025 | Diamond Infrastructure Solutions LLC (Minority) | Macquarie Infrastructure Partners | Renewable Energy & Infrastructure |

| 40 | 8/29/2025 | Pave America, LLC | AEA Investors LP; BC Investment Management Corporation | General Contractors & Heavy Civil Construction |

Let's Talk

Contact our Construction Industry Experts