This page was updated in August 2024 to enhance readability and accessibility. All content from the newsletter is now fully integrated into this page, allowing readers to access the information directly here.

Overall M&A Market Commentary

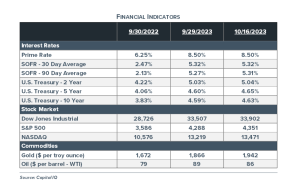

Interest rates are higher than before and now the hot topic in business conversation. After more than a decade of the Fed’s post “Great Recession” near-zero interest rate policy, we are suddenly in new economic territory. The Fed has hiked interest rates 11 times, producing an aggregate increase of 550 basis points in less than 18 months. This has resulted in the Prime Rate currently at an eye-popping 8.5%.

Even with these Fed inflation-fighting interest rate hikes, inflation has recently reversed its downward trend and moved a little higher. The recently released September CPI report put annualized inflation at 3.7%, equal to August’s 3.7% inflation and up from a low of 3.0% in June 2023. These values are well above the Fed’s 2.0% target and show how difficult it is to reduce inflation once it becomes embedded in the economy. Making matters worse, the UAW and other labor strikes coupled with the wars in Ukraine and now the Middle East could affect food and energy prices leading to even more inflation in the future. These events will make the Fed’s job of fighting inflation even more difficult. It looks like reaching the 2.0% inflation goal now becomes an even more strenuous endeavor.

While the Fed paused its interest rate hike in September (and may do so again in November), there is an increasing probability we will see another 50-basis point increase in December 2023. Whether or not an additional increase is made later this year, the important takeaway from the recently released minutes of the September 2023 Fed Open Market Committee was that interest rates could remain higher for longer. The business community survived higher interest rates decades ago well before the Great Recession. This time, the speed at which interest rates have risen has been difficult to digest and has created a daisy chain of significant impacts across the economy.

Rapidly rising rates contributed to the mini banking crisis earlier this year where several banks failed because of bank depositor runs due to a mismatch in their investment assets and funding liability mixes. These bank failures led to increased regulatory scrutiny of banks and a more conservative lending climate. Higher interest rates and more conservative lending lead to slow business investment and have a negative impact on the M&A market and economic growth.

Interest rates have not only affected businesses and the M&A market. The U.S. Government is a large creditor, with $33.5 trillion in debt, a record level. Currently, the national debt sits at 122.0% of GDP, the highest ratio of debt to GDP since World War II when the U.S. was funding the global war against the Axis Powers. Tudor Investment founder and early hedge fund pioneer, Paul Tudor Jones remarked on CNBC’s Squawk Box in early October, “As interest costs go up in the United States, you get in the vicious circle, where higher interest rates cause higher funding costs, cause higher debt issuance, which causes further bond liquidation, which causes higher rates, which puts us in an untenable fiscal position.” According to the Congressional Budget Office, the FY23 (ended September 30) Federal Deficit was $1.7 trillion, up 23.0% from FY22. According to the Committee for a Responsible Federal Budget, that deficit was “larger than any year in history in which we did not face a war, recession, or other major emergency.” According to the Congressional Budget Office, the Federal government paid nearly $0.66 trillion in interest in FY23 out of the $6.0 trillion total budget. We are on an unsustainable path as a country, especially if we want to continue funding war efforts in Ukraine and now in Israel and the Middle East.

The National Federation of Independent Business (“NFIB”) Small Business Optimism Index released in early October was down in September, marking the 21st consecutive month that the index was below the Index average. Inflation and labor quality were cited as the top concerns of small businesses. “Owners remain pessimistic about future business conditions, which has contributed to the low optimism they have regarding the economy,” said Bill Dunkelberg, NFIB Chief Economist. Further, he said, “Sales growth among small businesses has slowed and the bottom line is being squeezed, leaving owners few options beyond raising selling prices for financial relief.”

Consumer spending makes up about 70.0% of the Gross Domestic Product and is therefore the driver of the U.S. Economy. The University of Michigan Surveys of Consumers plunged in September 2023, falling to 63.0 from a value of 68.1 in the previous month. According to Joanne Hsu, the survey’s director, “Assessments of personal finances declined about 15%, primarily on a substantial increase in concerns over inflation, and one-year expected business conditions plunged about 19%.”

Consumers will continue to spend as long as they are comfortable that they will remain employed. Consumers are using credit cards to sustain their spending. In August 2023, consumer credit card debt surpassed $1 trillion for the first time even with record high credit card interest rates averaging 22.6%. A large portion of this spending is on nonessentials like clothing and travel which can be reduced quickly by the consumer. However, the level of consumer credit card debt is likely unsustainable and could influence the future growth in spending.

Even with all of this, the current slow deal environment could be potentially positive for some sellers. The private equity (“PE”) firms have abundant, time-limited investment capital to put to work. Furthermore, strategic buyers are still looking for growth opportunities and their businesses are in a strong financial condition. Where there is demand for deals, there is opportunity for sellers. The M&A market is always receptive to superior quality companies. We continue to be in a “flight to quality market” where buyers have a keen interest in high-quality companies. While this is no longer a seller’s market, there is still an opportunity to sell solid businesses. Well-prepared companies with sound business fundamentals will command broad buyer interest.

Due to the extended period over which private company M&A market data is collected, there is a one-quarter lag in our information. As a result, the market commentary reflected below is limited to the data through the second quarter of 2023. Any 3Q23 data included in this edition to expand trend lines is still preliminary and will be reviewed in detail in the next quarterly newsletter.

M&A Market Activity

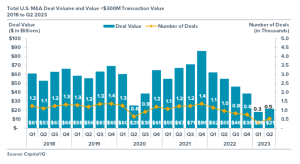

While down compared to mid-year 2022, M&A Deal activity through mid-2023 showed a pick-up in activity from 1Q23. The quick post COVID recovery led to excessive demand for goods and services and strong inflationary pressure. This inflation pressure was made worse by well-intentioned but poorly timed government spending and a flood of liquidity provided to businesses and individuals after the COVID recovery was well underway. Rapid Fed interest rate increases in 2022 and continuing into 2023 were meant to slow economic activity and stem the inflation problem. Higher interest rates have started to slow the economy but have not yet caused an economic recession. Companies and individuals are growing accustomed to higher interest rates and adjusting their behavior to accommodate these higher interest burdens. Higher interest costs are leading to lower business valuations and a pullback by PEs and other sellers that can delay and time their entry into the M&A market. This is leading to reduced M&A deal volumes in 2023 when compared to 2022 and 2021.

- $21.0 billion of middle-market deals was recorded in 2Q23, up 16.7% from the value in 1Q23 and in year-over-year comparisons, 2Q23 deal value was down 61.8% compared to 2Q22.

- The number of middle-market deals closed in 2Q23 was up 66.7% from the number of deals closed in 1Q23. 2Q23 deal volume was down 50.0% compared to 2Q22.

- The average middle-market deal size of $42.0 million in 2Q23 was smaller than the average $55.0 million deal size closed in 2Q22 and lower than the average deal size of $60.0 million recorded in 1Q23. The current M&A market has a greater number of smaller deals, perhaps reflecting the lower business risk and an easier path to obtaining financing for these smaller opportunities.

The 2Q23 PE exit data showed a similar trend of declining deal activity when compared to the overall M&A market. PE exit

activity measured by the number of deals was down 28.3% year over year, while the dollar value of PE exits was down 35.2% for the same period. Generally, PE sellers are less emotional about their company sales and able to time their exits to take advantage of market opportunities when they arise.

While the M&A market is seeing diminished activity, both strategic and financial buyers continue to be hungry for deals and are active participants in the M&A market. However, elevated borrowing costs and increased business uncertainty are creating pressure on buyers. With the low volume of new M&A deals, sellers with quality companies that enter the current market are receiving strong attention. Companies with solid performance and sellers who are prepared to manage the challenges of a more rigorous M&A process can still attract buyers and achieve high enterprise valuations.

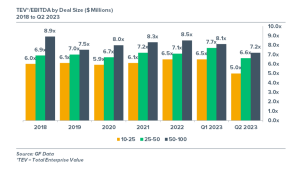

Middle Market Deal Valuations

Middle-market M&A valuations were surprisingly resilient going into 2023. For a while, the decline in new deal activity caused a supply-demand imbalance, which helped sustain higher post-pandemic deal valuations. Further, the late 2022 and early 2023 flight to quality in deal activity, where only high-quality deals closed, created an additional upward bias in M&A deal valuations. However, the Fed’s inflation fight, which led to a rapid aggregate 5.50% increase in interest rates in less than 18 months, is overwhelming the high valuation levels and is starting to push valuations lower.

Valuations started their decline in 2Q23, reflecting increased business uncertainty and higher interest rates. Valuations have declined across the deal size spectrum as buyers have begun to adjust their valuation offers to the elevated interest rate environment. While there is still a significant amount of available PE capital and large numbers of well-capitalized strategic acquirors, their unsatisfied deal appetite is not enough to continue to support valuations at elevated levels in a rapidly rising interest rate environment.

There is a growing “bid-ask spread” in the M&A market. Sellers are still wanting the inflated valuations of the immediate post-COVID period, while buyers are expecting to pay inflation and higher interest rate-adjusted valuations of the current deal market. It appears that the buyers are beginning to prevail in what is becoming a buyers’ market.

- Deal valuation multiples for the sub-$25.0 million category in 2Q23 came in at 5.0x, well below the long-run average of 6.1x for this size category, reflecting business uncertainty and increased financing costs.

- Deal valuation multiples for the large middle market, the above $50.0 million category, came in at 7.2x in 2Q23, well below the long-run average of 8.2x for this size category.

- Similarly, the valuations in the $25.0 to $50.0 million middle segment have declined to 6.6x, a level well below the five-year average of 7.0x.

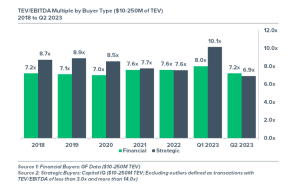

Private Equity versus Strategic Valuations

During the last decade, over 70.0% of all M&A deals were closed by strategic acquirors, including PE-owned strategics. Synergistic cost savings, access to new customers, and other revenue opportunities provide strategic buyers with the ability, but not the need, to pay more than the typical financial buyer. Over the last two years, the strategic community has backed away from paying the strategic premium. Our 1Q23 data showed a brief reversal of that trend, but 2Q23 indicates that the strategic community has once again backed away from paying the strategic premium. Furthermore, the 2Q23 data shows both financial and strategic buyers are starting to pay less for acquisitions.

- Strategic buyers are always active participants in middle-market M&A. In the post-pandemic years of 2021 and 2022, strategic buyers—on average—paid little strategic premium versus PEs for their acquisitions. Our 2Q23 data shows a continuation of that trend. In 2Q23, strategic buyer valuations of 6.9x were well below the 5-year trend level of 8.3x.

- Over the last five years, EBITDA multiples paid by PE buyers have remained in a range centered around 7.3x. The 2Q23 valuation data indicates that PEs are currently paying at trend level for new deals.

- Historical valuation data suggest that in the M&A market, strategic buyers tend to pay a premium of about 1.5x when compared to PE firms. The 2Q23 data indicates that the strategic premium is zero, well below the average premium levels of the last 5 years.

- Prairie estimates that, for deals below $50.0 million, middle-market valuations are one to two multiples of EBITDA lower than the levels reflected in the chart below.

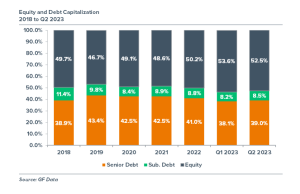

Middle Market Leveraged Buy Out Capitalizations

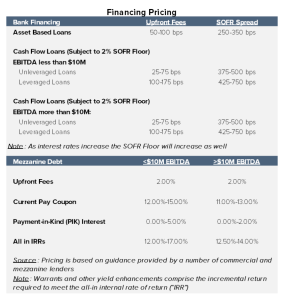

There is a reduction of debt leverage in current capital structures. Middle-market company capitalizations are more conservative as lenders incorporate the effects of more business uncertainty, sustained inflation issues, and higher financing costs in their lending proposals. Bank credit is becoming harder to obtain as banks and other lenders have tightened their credit parameters. According to the July 2023 Fed Senior Loan Officer survey, during 2Q23 there was a move toward tighter lending standards, and banks were seeing weaker demand for commercial and industrial (C&I) loans across all company size ranges. Tighter standards coupled with increased interest costs lead to lower loan demand and debt becoming a smaller component of a typical leveraged deal capital structure. Business development corporations (“BDCs”) and mezzanine lenders have bridged the gap in loan availability, but even these capital sources continue to reduce their holds, increase their interest rates, and are requiring more lender-friendly terms.

- Loan availability is reduced in the current market, and the lending terms are becoming more conservative. Acquisition deals are seeing less financial leverage, higher interest costs, and more stringent terms, reflecting overall increased business risks in the current environment. Currently, debt is well below 50.0% of a typical capital structure.

- BDCs have been strong participants in the deal market, especially for larger deals. But while they are becoming more active in the market, their loans are more expensive. Further, the BDCs tend to focus on deals with private equity funds.

- Mezzanine funds are active in leveraged transactions. This capital has a high interest rate that can stress a company’s cash flow. Mezzanine is increasingly a critical component of a middle-market buyout capital structure when senior debt capital is harder to find. Interest-only and payment-in-kind (“PIK”) structures still dominate the markets, but in the current environment, the use of equity co-investment structures helps match mezzanine returns with deal risk profiles.

Overall Comment on the Financing Markets

Increased interest rates have affected businesses, consumers, and state and local governments. Interest rates have moved 550 basis points higher in less than 18 months, causing stress across all sectors of the economy. While interest rates have been at these or higher levels in the past, the speed at which interest rates have climbed is the issue. Since the “Great Recession” in 2010, the economy has subsisted on a near-zero interest rate environment. This “free debt” mentality has altered the behavior of many corporate executives and individuals. Corporate executives and PE partners who are younger than 40 have not had to deal with interest rates at these elevated levels. The whole concept of the prudent use of debt and covering debt service is now changing and reentering corporate borrowing regiments and M&A deal structures.

Because of the effects of inflation on purchasing, a combination of increased capital costs from the higher interest rates and lower free cash flow is straining the ability of borrowers to service their debt. As described earlier, the September 2023 Fed Senior Loan Officer Survey indicates that commercial banks are tightening their lending parameters and moving to a more “risk-off” mode for new loans. Higher interest rates and debt service costs are leading to increased new project investment hurdle rates and thus lower demand for debt to finance corporate projects. Less corporate borrowing coupled with fewer M&A deals is leading to lower new loan demand by issuers. Through the first three quarters of 2023, U.S. leveraged loan issuance is down 23.0% compared to the same period last year. Oftentimes, a more conservative credit environment is a precursor to a future recession.

The consumer price index (“CPI”) released on October 12th for September was 3.7%, unchanged from August and rising from 3.2% in July and 3.0% in June, which was the inflation low water mark. This trend is not what the Fed is looking for and indicates how embedded inflation is in our economy. Inflation erodes the purchasing power of consumers and businesses alike and impacts the growth and efficiency of the economy.

In the Fed September 2023 Open Market Committee meeting, interest rates were left unchanged, leaving the target range of 5.25% – 5.50% at a 22-year high. In remarks after the meeting, Fed Chairman Powell indicated that the Fed is forecasting “higher rates for longer,” well into 2024 and 2025 because of a strong labor market, persistent inflation, and a surprisingly resilient economy. Furthermore, a suggestion was also made that there could be an additional 50 basis point increase in interest rates in one of the two remaining Open Market Committee meetings this year. Higher interest rates are beginning to drag on the M&A market and could further challenge the market.

Financing has become more expensive in 2023 and M&A valuations are beginning to be negatively impacted. While financing for deals is still available, it is more expensive and more difficult to obtain. Preparation is key in this market. All borrowers should have documented business contingency plans that show lenders how the company will react to higher interest rates, lower margins, changes to revenues, and other business issues. Lenders want to be repaid, so borrowers must detail how they will make that happen. With proper preparation and good quality, credit-worthy issuers should be able to attract capital. Borrowers will have to be prepared for an extended financing process and potentially more conservative and expensive capital structures.

Total U.S. Middle Market Loan Issuance

- U.S. Leveraged Loan issuance in 2022 at $850.0 billion dropped about 35.0% from the record volume of $1.31 trillion recorded in 2021. The loan volume decline continued well into 2023, as 3Q23 new Leveraged Loan Issuance declined more than 23.0% from the issuance in 3Q22. With the current conservative lending environment, further declines in leading volume are expected toward the end of 2023.

- The Fed took the necessary steps to support banks and maintain sufficient liquidity in the banking system during the pandemic. That strategy succeeded, resulting in abundant liquidity for loans in the banking system. However, higher interest rates coupled with market uncertainty create an environment where lenders are more cautious and have reduced their appetite for new leveraged loans in 2023.

- Bank lenders continued to focus on relationship banking, corporate borrowers’ lines of credit, and areas where they have a competitive advantage, such as operating business needs (including payroll and checking accounts). Due to the current economic environment, banks are cautious in making new loans and are very selective in new leveraged transactions. BDCs and other lenders have taken up the slack, but even this sector is less aggressive than previously.

Interest Rate Environment

Interest rates have moved higher from January 2022, when the Prime Rate stood at 3.25%, to the end of 3Q23, where the Prime Rate is now 8.50%. This rapid 525 basis point interest rate increase over six quarters was due to the Fed’s efforts to reduce stubborn inflation in the economy. Inflation hit a high of 9.1% in June 2022 because of the bid-up in prices due to shortages of goods and services created by the rapid economic recovery from the COVID lockdowns. Furthermore, the government’s use of copious amounts of well-intended, but excessive, stimulus checks and recovery spending further increased the inflationary pressures.

While these interest rate increases helped move inflation lower in 2023, where the CPI reached a low point of 3.0% in June 2023, it reversed course and hit 3.7% in August and September 2023. Stubborn inflation could lead to additional rate increases later in 2023 and 2024 and/or an extended period of sustained higher interest rates. In late September, a Fed governor said, “The most important question at this point is not whether an additional rate increase is needed this year or not, but rather how long we will need to hold rates at a sufficient restrictive level to achieve our goals.”

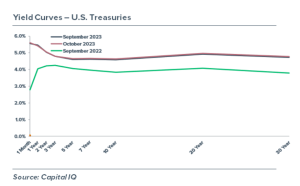

As a result of the Fed interest rate increases, the yield curve shifted higher and continues to be inverted. The slope of the yield curve at the end of 2021 was upward sloping, reflecting increasing but, at that time, normal inflation expectations. The 2-year to 10-year Treasury differential was a positive 79 basis points at the end of 2021. At the end of 2022, because of the Fed’s unusual manipulations of the short-term Fed Funds Rate, that differential was shifted to a negative 53 basis points, resulting in an inverted yield curve. At the end of 2Q23, the 2-year to 10-year differential was at a negative 58 basis points and a negative 44 basis points at the end of 3Q23. While not perfect, an inverted yield curve is a reliable predictor of a recession in the future, although how far in the future is the question.

Middle Market Debt Multiples

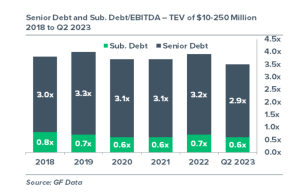

- Average total debt leverage in middle-market deals moved lower in 2Q23 to 3.5x, up from the 3.7x average in the 2020 and 2021 period. As noted earlier, the current business uncertainty is leading to lower debt leverage in 2023.

- Mezzanine capital continues to play a key role in leveraged capital structures. While mezzanine is more expensive capital than senior debt, its return structure matches the risk profile of companies operating in the current uncertain economic environment.

- Over the past five years (2018-2022), mezzanine debt averaged about 0.7x EBITDA in the typical capital structure. In the post pandemic period, with an increasingly conservative bank lending environment, mezzanine capital may become a more significant component of the typical capital structure, but as of 2Q23 has not done so.

- A more conservative senior debt lending markets and continuing Fed interest rate increases during 2023 has already started to negatively impact the amount of senior debt in the typical capital structure.

Terry Bressler is a Managing Director and can be contacted at 312.348.1323 or by email, tbressler@prairiecap.com.

Download the full article above.